Imagine you lose your job tomorrow. Or your car breaks down and needs ₹50,000 in repairs. Or a family member needs emergency hospitalisation and your insurance does not cover everything upfront. How would you handle it without going into debt or selling your investments at a loss? That is exactly what an emergency fund is for. It is the financial safety net that keeps the rest of your money plan intact.

What is an emergency fund?

An emergency fund is a separate pool of money set aside specifically for unexpected expenses or a sudden loss of income. It is not for vacations, gadgets, or home renovation. It is purely for genuine emergencies.

Think of it as insurance for your financial life — you hope you never need it, but you will be extremely grateful it is there when you do.

How much should you save?

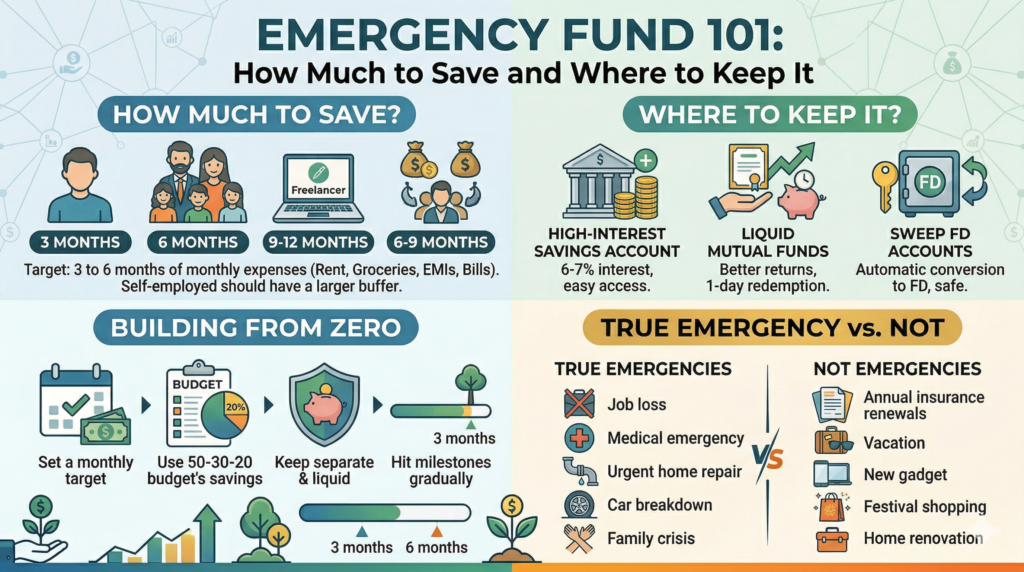

The standard recommendation is to save 3 to 6 months of your monthly expenses as your emergency fund.

Note: this is expenses, not income. If your monthly expenses (rent, groceries, bills, EMIs, school fees) total ₹40,000, your target emergency fund is ₹1.2 lakh to ₹2.4 lakh.

Here is a simple guide based on your situation:

– Single, no dependents, stable job → 3 months of expenses

– Married, one income, children → 6 months of expenses

– Self-employed or freelancer → 9 to 12 months of expenses

– Multiple loans or high fixed commitments → 6 to 9 months

If you are self-employed or run a business, income can be irregular, so a larger buffer is essential.

Where should you keep your emergency fund?

Your emergency fund must be:

– Liquid: You should be able to access it within 24–48 hours

– Safe: No market risk — the principal should never lose value

– Separate: Not mixed with your daily account, so you are not tempted to spend it

Here are the best options in India:

1. High-interest savings account: Some small finance banks (like AU Small Finance Bank, IDFC First) offer 6–7% interest. Easy access, safe, and earns decent returns.

2. Liquid mutual funds: These invest in very short-term debt instruments and can be redeemed within 1 business day. Better returns than savings accounts, similar safety. Platforms like Groww or Zerodha Coin make this easy.

3. Sweep FD accounts: Some banks offer accounts where excess balance is automatically converted to FD and broken back when needed.

Avoid keeping your emergency fund in equity mutual funds, stocks, or PPF — these are either market-linked or illiquid.

How to build it if you are starting from zero

Do not wait until you have the full amount saved before you feel secure. Start small and build it gradually.

A simple approach:

1. Set a monthly target — even ₹2,000 to ₹5,000 per month helps

2. Use your 50-30-20 budget’s savings bucket to fund it first

3. Keep it in a liquid fund or separate savings account

4. Hit the 3-month milestone first, then build towards 6 months

5. Treat it as a non-negotiable monthly transfer, like an EMI to yourself

If you receive a bonus, festive gift, or tax refund, consider directing a portion directly into the emergency fund.

What counts as a real emergency?

This is important, because many people raid their emergency fund for things that are not true emergencies.

True emergencies:

– Job loss or sudden reduction in income

– Medical emergency not fully covered by insurance

– Urgent home repair (flooding, structural damage)

– Car breakdown needed for work

– Family crisis requiring immediate funds

Not emergencies (plan separately for these):

– Annual insurance renewals

– Vacation

– New phone or laptop

– Festival shopping

– Home renovation

For predictable large expenses, maintain a separate sinking fund — a small monthly savings specifically for that goal.

What do you do after you use it?

If you ever dip into your emergency fund, replenish it as quickly as possible. Treat the rebuilding as a priority, just like an EMI.

Your emergency fund is the foundation of your entire financial plan. Without it, any unexpected event can derail your investments, force you into debt, or make you liquidate long-term assets at the wrong time.

The bottom line

Before you invest a single rupee in mutual funds or stocks, make sure you have at least one month of expenses saved as a buffer. Then build towards 3 to 6 months systematically.

An emergency fund is not exciting — it does not appear on investment trackers or leaderboards. But it is the most important financial safety net you will ever build.