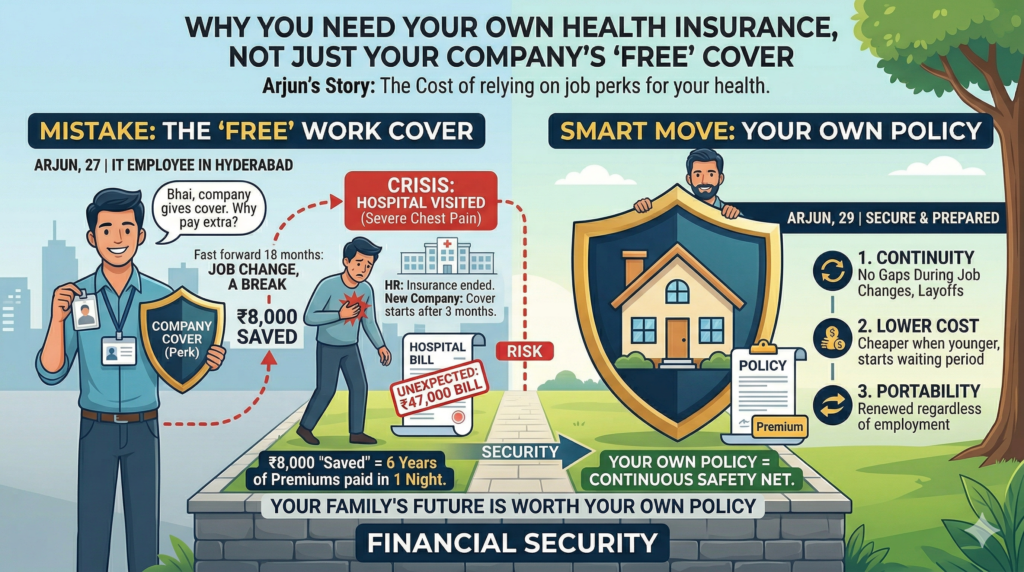

Arjun was 27, freshly placed at a good IT company in Hyderabad, and proud of his budgeting skills. He tracked every rupee. He had a SIP running. He avoided unnecessary expenses.

When a colleague suggested buying a personal health insurance plan, Arjun smiled and said, “Bhai, my company already gives me cover. Why would I pay extra for the same thing?”

It made complete sense. ₹8,000 a year saved. Smart move, right?

Fast forward eighteen months

Arjun got a better offer. Excited, he put in his papers and decided to take a month off before joining the new company. A well-deserved break after two years of hard work.

Three weeks into that break, he woke up at 2 AM with severe chest pain. His roommate rushed him to a nearby hospital. Tests, monitoring, an overnight stay — thankfully nothing serious. But the hospital bill said otherwise.

₹47,000. For one night.

“I called my HR. They said my insurance ended on my last working day. I called the new company. They said my cover starts after probation — three months away.”

— Arjun, paying ₹47,000 out of pocket

That ₹8,000 he had “saved” every year? He paid six years’ worth of premiums in a single night — with zero coverage.

The thing nobody tells you about “free” health cover

Arjun’s story is not rare. It plays out quietly, in cities across India, every single day. A job change, a layoff, a sabbatical, a startup leap — and suddenly there is no safety net.

The “free” health cover at work was never really yours. It was a perk — useful while it lasted, but gone the moment your employment ended. No warning. No extension. Just a gap, right when you are most vulnerable.

And healthcare costs in India are rising fast. A basic hospitalisation today easily runs into tens of thousands. A surgery or ICU stay? Lakhs. Your savings — the ones you worked so hard to build — can disappear in days.

What Arjun did next

The day he joined his new company, Arjun bought his own health insurance policy. ₹10 lakh cover. Portability intact. Renewed every year, regardless of where he works.

He also started the waiting period clock — something he wishes he had done at 25, not 29.

The lesson Arjun learned the hard way

A personal health insurance plan is not a duplicate expense. It is your own safety net — one that stays with you through every job, every gap, and every phase of life. The earlier you get it, the cheaper and more valuable it becomes.

You are not Arjun. You still have time to make a different choice.