Most people either have too little life insurance or none at all. A few have so much that they are paying far more than necessary. Getting the right amount of cover is one of the most important financial decisions you will make — because it is not about you. It is about the people who depend on you.

Why do you need life insurance?

Life insurance exists to replace your income if you die unexpectedly. If you are the primary earner in your family, your sudden absence would leave your family without their main source of income — at a time when they are already grieving.

A good life insurance policy ensures that your family can:

– Pay off your home loan or other debts

– Continue their current lifestyle

– Fund your children’s education

– Not be forced to sell assets under pressure

This is why term insurance — the purest and most affordable form of life insurance — is essential for every earning adult with dependents.

How much cover do you actually need?

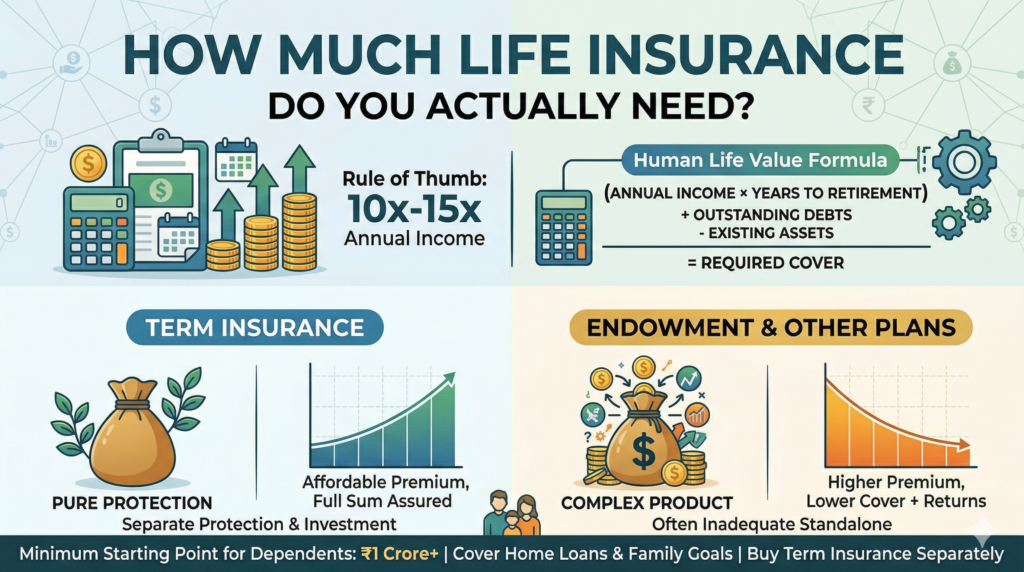

A simple and widely used rule of thumb is to have life cover equal to at least 10 to 15 times your annual income.

So if you earn ₹10 lakh per year, you should ideally have a cover of ₹1 crore to ₹1.5 crore.

But this is just a starting point. The right amount depends on several personal factors.

The Human Life Value (HLV) approach

A more precise method is the Human Life Value approach, which considers:

1. Your current annual income

2. Number of years left until retirement (e.g., if you are 30 and plan to retire at 60, that is 30 years)

3. Your annual expenses and the share your family depends on

4. Your existing assets (savings, investments, existing insurance)

5. Outstanding liabilities (home loan, car loan, personal loan)

Formula: Required cover = (Annual income × Years to retirement) + Outstanding debts − Existing assets

For example: ₹10 lakh × 25 years + ₹30 lakh home loan − ₹15 lakh savings = ₹2.65 crore

What about existing policies?

Many people have endowment policies or LIC policies their parents took out for them. These typically offer very low cover — sometimes just ₹5 lakh to ₹10 lakh.

These are not adequate as standalone life insurance. You may need a separate term plan to fill the gap.

Also count any employer-provided group life cover, but remember that this cover ends when you change jobs.

Term insurance vs other life insurance products

Term insurance is pure protection — you pay a premium, and your family gets the full sum assured if you die within the policy term. No maturity benefit, no investment component. And because of that, it is extremely affordable.

For example, a healthy 30-year-old can get a ₹1 crore term cover for as little as ₹8,000–₹12,000 per year.

Other products like ULIPs and endowment plans combine insurance with investment, but typically offer poorer returns than mutual funds and inadequate insurance coverage. For most people, the smarter approach is to buy term insurance separately and invest separately.

A practical checklist

Before buying, ask yourself these questions:

1. How much does my family need per month to maintain their lifestyle?

2. How many years of income do I need to replace?

3. What loans would need to be repaid?

4. What financial goals (education, marriage) do I want to secure?

5. What assets do I already have that could support my family?

The answers will give you a clear picture of the right cover amount.

The bottom line

The right life insurance cover is personal — but the starting point for most earning adults with dependents is ₹1 crore minimum. If you have a home loan, children, or aging parents depending on you, aim higher.

Buy early, buy enough, and choose a reputable insurer with a strong claim settlement ratio. Your family is counting on you to get this right.