When you decide to invest in mutual funds, one of the first questions you face is: should I invest a fixed amount every month (SIP), or should I put in all my money at once (lump sum)? This is one of the most common questions first-time investors ask, and the answer depends on your situation. Let us break it down simply.

What is a SIP?

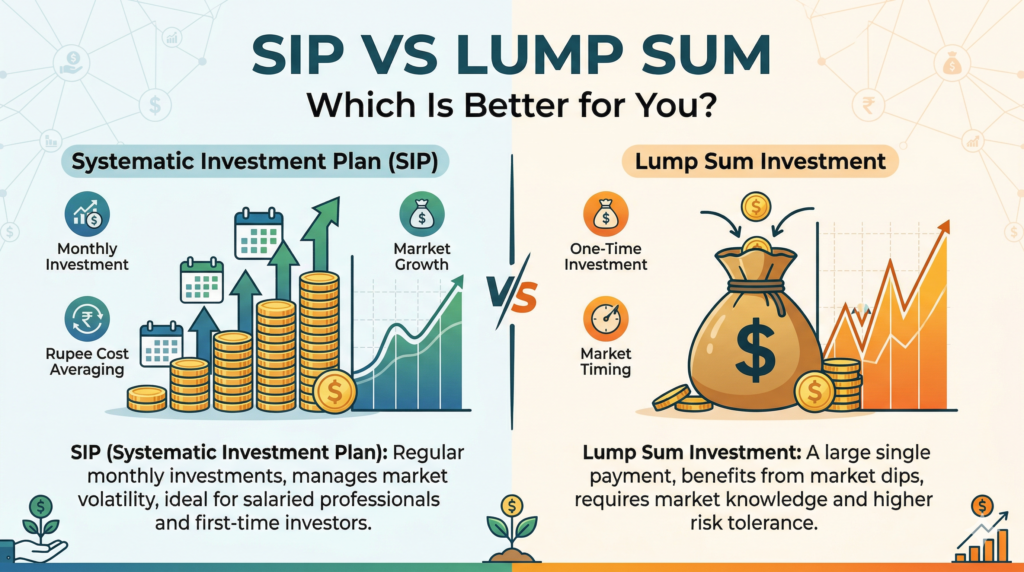

SIP stands for Systematic Investment Plan. It means investing a fixed amount — say ₹5,000 — into a mutual fund automatically every month, on a pre-set date.

Think of it like an EMI, but instead of paying a loan, you are building wealth.

Example: If you start a SIP of ₹5,000 per month in an equity mutual fund and continue for 15 years at an average 12% annual return, you would accumulate approximately ₹25 lakh from a total investment of just ₹9 lakh.

What is a lump sum investment?

A lump sum investment means putting in a large amount all at once — for example, investing ₹1 lakh into a mutual fund in one go.

This is common when someone receives a bonus, an inheritance, the proceeds from selling a property, or a large salary payout.

The key difference: Rupee Cost Averaging

The biggest advantage of SIP is something called rupee cost averaging.

Because you invest every month regardless of market conditions, you automatically buy more units when prices are low and fewer units when prices are high. Over time, this averages out your purchase cost and reduces the impact of market volatility.

With a lump sum, timing matters a lot. If you invest ₹1 lakh when the market is at its peak and the market falls 20% soon after, your investment is immediately worth ₹80,000. If you had spread that ₹1 lakh over 10 months instead, your average cost would be lower.

When is SIP better?

SIP is the better choice for you if:

– You are a salaried professional with a regular monthly income

– You do not have a large lump sum to invest right now

– You are new to investing and want to reduce risk

– Your goal is long-term wealth creation (5–20 years)

– You want a disciplined, automatic investing habit

For most salaried individuals and first-time investors, SIP is the recommended starting point.

When is lump sum better?

Lump sum investing can work well if:

– You have a large amount available (bonus, maturity proceeds, gift)

– The market has just seen a significant correction (prices are low)

– You have a long investment horizon of 7+ years

– You are experienced enough to handle short-term volatility without panic

Even then, a common strategy is to park the lump sum in a liquid fund first and then transfer it into equity funds over 6–12 months through a Systematic Transfer Plan (STP) — getting the best of both worlds.

Can you do both?

Absolutely — and many smart investors do exactly that. You can run a monthly SIP for regular savings and make additional lump sum investments during market corrections or when you receive a bonus.

The two approaches complement each other well.

The verdict

For most people reading this, especially if you are starting out, SIP is the way to go. It is simple, automatic, requires no market timing, and builds a powerful long-term habit.

Start with whatever amount you are comfortable with — even ₹500 a month — and increase it as your income grows. The best time to start a SIP was yesterday. The second best time is today.