Most people either budget obsessively or not at all. If you have ever tried to track every single rupee you spend and given up after a week, you are not alone. The good news is that you do not need a complicated spreadsheet to manage your money well. The 50-30-20 rule is one of the simplest and most effective budgeting methods in the world — and you can start using it today.

What is the 50-30-20 rule?

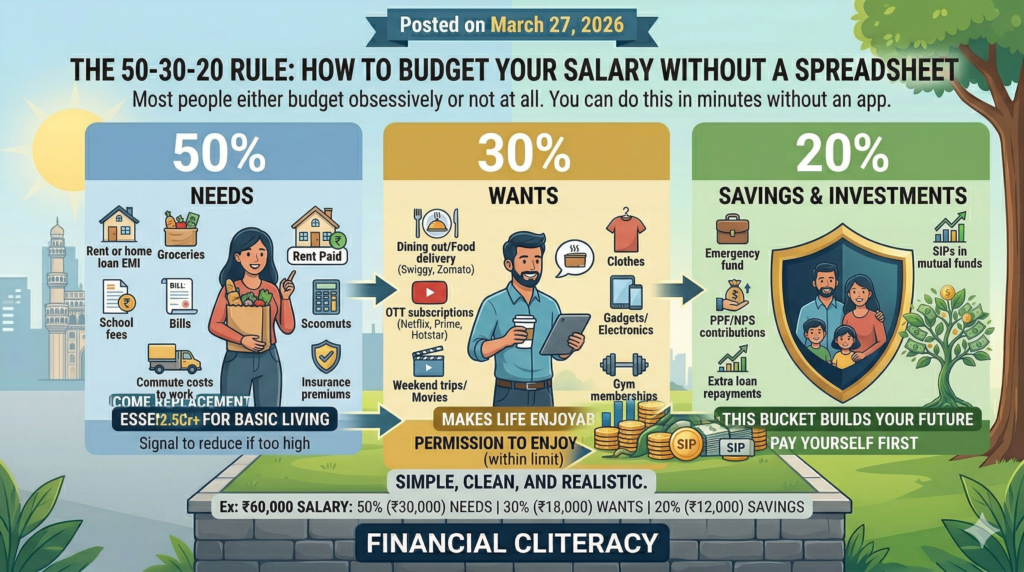

The 50-30-20 rule was popularised by US Senator Elizabeth Warren in her book ‘All Your Worth’. It divides your take-home salary into three simple buckets:

50% — Needs

30% — Wants

20% — Savings and investments

That is it. No detailed category tracking. No guilt about buying a coffee. Just three numbers.

What counts as a Need? (50%)

Needs are expenses you cannot avoid — things that are essential for your basic living.

Examples:

– Rent or home loan EMI

– Groceries and cooking gas

– Electricity and water bills

– Internet and mobile bills

– School fees for children

– Commute costs to work

– Insurance premiums

– Minimum debt repayments

If your needs exceed 50% of your salary, that is a signal to look for ways to reduce fixed costs — maybe renegotiating rent, cutting unnecessary subscriptions, or refinancing a loan.

What counts as a Want? (30%)

Wants are the things that make life enjoyable but are not strictly necessary.

Examples:

– Dining out and ordering food online (Swiggy, Zomato)

– OTT subscriptions (Netflix, Prime, Hotstar)

– Weekend trips and movies

– New clothes beyond essentials

– Gadgets and electronics upgrades

– Gym memberships

– Shopping on Myntra or Amazon

The 30% allocation gives you permission to enjoy your money without guilt — as long as you stay within the limit.

What goes into Savings and Investments? (20%)

This is the bucket that builds your future. It includes:

– Emergency fund contributions

– SIPs in mutual funds

– PPF or NPS contributions

– Term insurance and health insurance premiums (if not counted in needs)

– Stocks or other investments

– Extra loan repayments

Pay yourself first. Set up an automatic transfer to your savings account or SIP on the same day your salary arrives, before you get a chance to spend it.

Let us see it with real numbers

Suppose your take-home salary is ₹60,000 per month.

50% (₹30,000) → Rent ₹12,000 + Groceries ₹6,000 + Bills ₹3,000 + School fees ₹5,000 + Commute ₹2,000 + Insurance ₹2,000 = ₹30,000

30% (₹18,000) → Dining out ₹4,000 + Entertainment ₹3,000 + Clothes ₹3,000 + Weekend outings ₹4,000 + Misc ₹4,000 = ₹18,000

20% (₹12,000) → SIP ₹7,000 + Emergency fund ₹3,000 + PPF ₹2,000 = ₹12,000

Simple, clean, and realistic.

What if the numbers don’t fit neatly?

The 50-30-20 rule is a guideline, not a law. If you are paying off a large loan, your savings bucket might need to be larger temporarily. If you live in a metro city with high rent, your needs bucket might naturally exceed 50%.

The goal is to be conscious and intentional about where your money goes — not to achieve a perfect split every single month.

How to start today

Step 1: Find out your actual take-home salary (after all deductions).

Step 2: Calculate your three buckets — 50%, 30%, and 20%.

Step 3: Compare your current spending to these buckets.

Step 4: Identify the biggest leaks and address them one at a time.

Step 5: Set up an automatic SIP or RD transfer on salary day.

That is all it takes. No app required. No spreadsheet needed. Just three numbers and the discipline to follow them.