Section 80C is arguably the most important tax-saving provision in the Indian Income Tax Act. It allows you to reduce your taxable income by up to ₹1.5 lakh per financial year — potentially saving you ₹15,000 to ₹46,800 in taxes depending on your slab. But many people either do not fully use this deduction or use it inefficiently. Here is a complete guide.

Who can use 80C?

Section 80C is available to individual taxpayers and Hindu Undivided Families (HUFs) under the old tax regime. It is NOT available under the new tax regime.

Before maximising 80C, make sure the old tax regime is actually beneficial for you. If your employer offers the choice, compare both regimes based on your income and deductions.

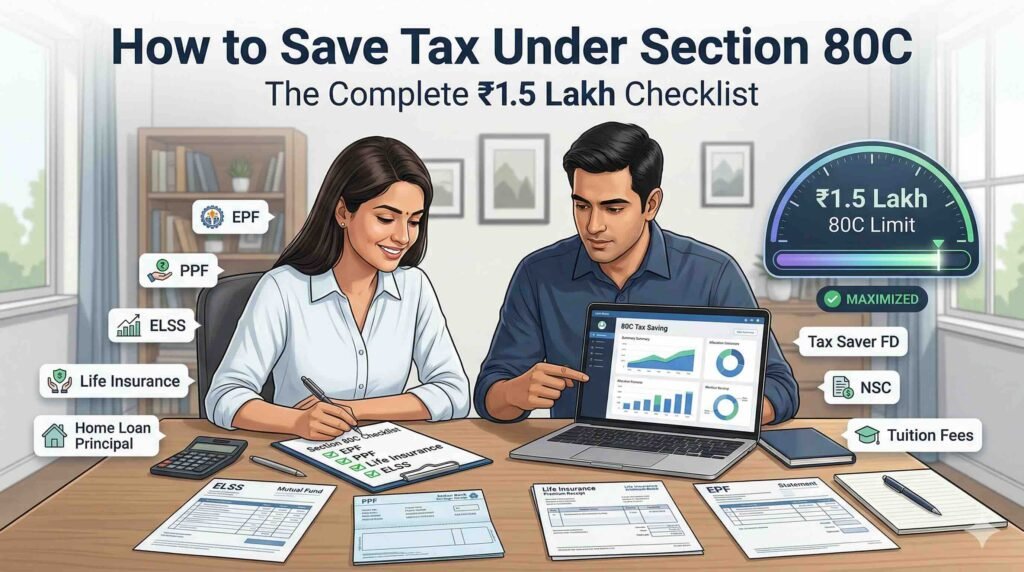

The complete list of 80C investments

Here are all the eligible investments and expenses under Section 80C:

Investments:

– ELSS (Equity Linked Savings Scheme) mutual funds

– PPF (Public Provident Fund)

– EPF (Employee Provident Fund) — your employee contribution

– NPS (National Pension System) — employee contribution to Tier-I account

– NSC (National Savings Certificate)

– 5-year Tax Saving Fixed Deposit (with any bank)

– Senior Citizens Savings Scheme (SCSS)

– Sukanya Samriddhi Yojana (for girl child)

– Life insurance premiums (for self, spouse, or children)

– ULIP premiums

Expenses that qualify:

– Home loan principal repayment

– Stamp duty and registration charges for a new home (in the year of purchase only)

– Children’s tuition fees (for up to 2 children, for full-time education in India)

Many people already use ₹1.5 lakh without realising it

If you are a salaried employee, your EPF contribution (12% of basic salary) counts towards 80C. If your basic salary is ₹25,000 per month, your EPF contribution alone is ₹36,000 per year.

If you are paying a home loan, the principal repayment counts too. A ₹40 lakh home loan’s principal component in the first year could be ₹60,000–₹80,000.

Combining EPF + home loan principal might already bring you close to ₹1.5 lakh — so you may only need to invest an additional ₹50,000–₹70,000 to fully utilise 80C.

The 80C checklist — step by step

Step 1: Check your EPF statement — how much did your employee contribution total this year?

Step 2: Add up any life insurance premiums you already pay.

Step 3: Add your home loan principal repayment (if applicable).

Step 4: Add children’s tuition fees (if applicable).

Step 5: Calculate: ₹1,50,000 − (sum of above) = remaining amount you need to invest.

Step 6: Invest the remaining amount in the most suitable option — ELSS via SIP if you want equity growth, PPF if you want safe guaranteed returns, or 5-year FD if you want capital protection.

Beyond 80C: other deductions to know

80D: Up to ₹25,000 for health insurance premiums (₹50,000 if covering parents above 60). This is separate from 80C and can be claimed additionally.

80CCD(1B): Up to ₹50,000 additional deduction for NPS contributions — over and above the ₹1.5 lakh 80C limit.

80E: Interest on education loan — fully deductible for up to 8 years.

24(b): Home loan interest — up to ₹2 lakh deductible for self-occupied property.

HRA exemption: Calculated separately and reduces taxable salary — not counted within 80C.

The bottom line

Section 80C alone can save you up to ₹46,800 per year (at 31.2% tax rate including cess). Add 80D and 80CCD(1B) and your total tax saving could cross ₹75,000 annually.

Start planning in April. Set up SIPs for ELSS in the first week of the financial year. Do not let this opportunity shrink into a last-minute March scramble.