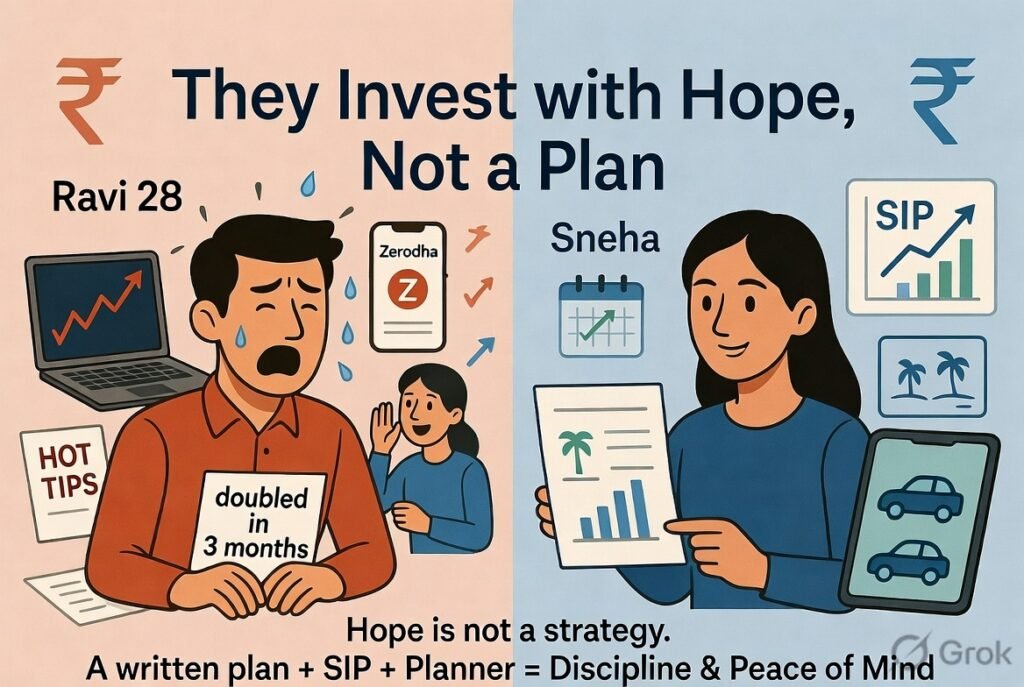

Ravi was 28 when he got his first real salary — ₹65,000 a month, credited on the 1st of March. By the 3rd, he had opened a Zerodha account. By the 5th, he had bought ₹40,000 worth of shares in a PSU stock his colleague Ankit had mentioned over lunch.

“Ankit doubled his money in three months,” Ravi told himself, refreshing his portfolio every hour. “Why shouldn’t I?”

Six months later, Ravi’s ₹40,000 was worth ₹27,000. Ankit, for what it’s worth, had sold his shares two days before Ravi bought them.

This is the most common way Indians lose money in the stock market — not through bad luck, but through investing with hope instead of a plan.

What Does “No Plan” Actually Look Like?

Ravi didn’t ask himself any of the questions that matter before investing: What is this money for? When will I need it? How much loss can I absorb without panic-selling? What will I do if the stock falls 30%?

Without answers to these questions, every investment decision becomes emotional. You buy when things look exciting. You sell when things look scary. And in between, you refresh your portfolio constantly, hoping the number goes up.

Hope is not a strategy. It is the absence of one.

The Alternative: Goal-Based Investing

Contrast Ravi’s story with Sneha, also 28, also earning ₹65,000 a month. Sneha sat down with a registered financial planner and mapped out three goals: a foreign vacation in 2 years (₹2 lakh needed), a car down payment in 4 years (₹3 lakh), and a retirement corpus for 30 years from now.

For each goal, her planner helped her choose the right tool: a recurring deposit for the vacation, a debt mutual fund for the car, and an equity SIP for retirement. She started with just ₹5,000 a month in a diversified equity fund — a fund her planner selected based on consistency and fit, not last year’s returns.

Three years later, Sneha’s vacation fund is intact. Her SIP has grown to ₹2.3 lakh. And she has never once panic-sold — not just because the plan makes sense, but because she has someone to call when the market falls and she starts to worry.

The Power of the SIP Structure

A Systematic Investment Plan forces you to invest a fixed amount every month, regardless of whether the market is up or down. Over 10 years at a conservative 12% annual return, ₹5,000 a month grows to over ₹11.6 lakh. That’s not magic — that’s compounding, applied with discipline.

More importantly, an SIP removes hope from the equation. You don’t need to predict the market. You don’t need a hot tip. You just need a goal, a timeline, and the patience to let the process work.

The Lesson

Before your next investment, write down three things: what the money is for, when you’ll need it, and how much you can afford to lose without sleeping badly. If you can’t answer all three clearly, you’re not investing. You’re gambling with extra steps. A financial planner helps you answer those three questions — and then builds a portfolio around the answers.

Ravi, by the way, eventually recovered. He connected with a financial planner who helped him channel his energy from stock-picking into a structured SIP plan. He still asks too many questions. His planner says that’s fine.

The Planner Advantage

This is exactly where a financial planner earns their keep — not by picking funds, but by sitting with you before you invest a single rupee and helping you build a goal map. What are you saving for? When do you need it? How much risk can you actually stomach? A good planner asks these questions systematically, translates your answers into an investment strategy, and gives you a written plan to refer back to when the market gets noisy. For most people, that structure alone is worth more than any single fund recommendation.