Most salaried professionals receive their salary slip every month and either glance at the final number or ignore it entirely. But your salary slip contains a wealth of information that directly affects your tax liability, take-home pay, and financial planning. Let us decode it together.

The two sides of your salary slip

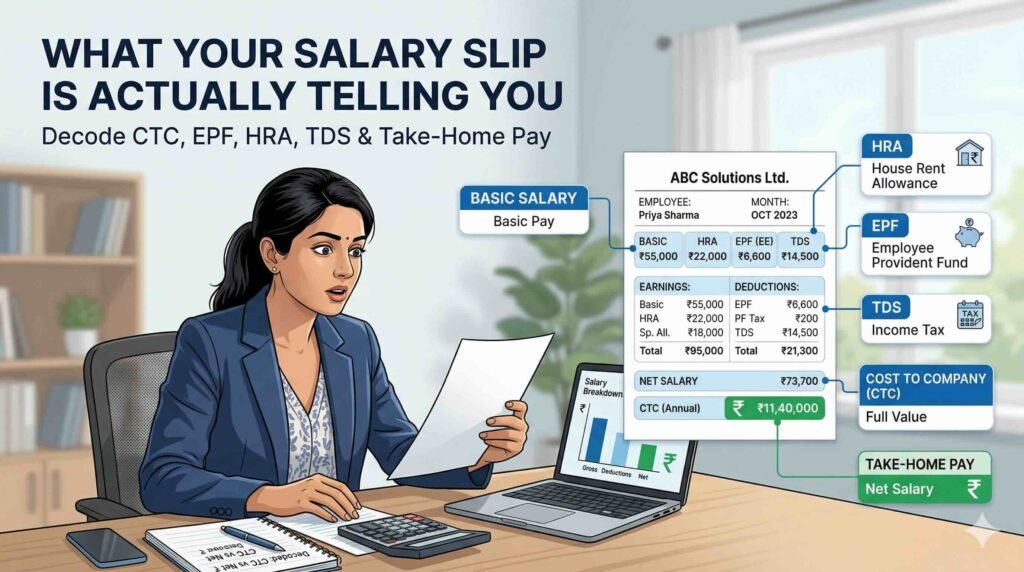

Every salary slip is divided into two parts:

1. Earnings (what your company pays you)

2. Deductions (what gets taken out before the money reaches your account)

Your take-home pay = Total Earnings − Total Deductions

Understanding the Earnings side

Basic Salary: This is the foundation of your salary. Usually 40–50% of your CTC (Cost to Company). It is fully taxable. Higher basic salary = higher EPF contribution = higher gratuity.

HRA (House Rent Allowance): This is paid to cover your rent. If you live in a rented home and submit rent receipts, a portion of HRA is tax-exempt. The exemption depends on your city, basic salary, and actual rent paid.

Special Allowance: This is the balancing figure that makes up the rest of your salary after all other components. It is fully taxable.

Conveyance / Transport Allowance: Partially or fully taxable depending on whether it is a standard allowance or reimbursement.

Medical Reimbursement: If given as reimbursement (with bills), it may be partially tax-exempt.

LTA (Leave Travel Allowance): Tax-exempt if you actually travel within India and claim it properly, twice in a 4-year block.

Bonus: Fully taxable. Included in your salary and taxed as per your slab.

Understanding the Deductions side

EPF (Employee Provident Fund): 12% of your basic salary is deducted and deposited into your EPF account. Your employer also contributes 12%. This is a retirement savings pool that earns 8.15% interest per year (current rate), fully tax-free.

Professional Tax: A state government tax, typically ₹200 per month. Deductible from taxable income.

TDS (Tax Deducted at Source): Your employer deducts income tax on your behalf and deposits it with the government. The amount depends on your salary, declared investments, and HRA exemption. If you do not submit your investment proofs on time, your employer deducts TDS at the maximum rate.

Group Insurance Premium: Some companies deduct a small amount for group health or life insurance provided by the employer.

What is CTC vs Gross Salary vs Take-Home?

This confuses many people:

CTC (Cost to Company): The total annual cost your employer incurs for you. This includes your salary, employer’s EPF contribution, gratuity provision, and any other benefits. This is always the highest number.

Gross Salary: Your total earnings before deductions. Lower than CTC because it excludes employer’s contributions.

Net Salary / Take-Home: What gets credited to your bank account after all deductions. This is the lowest number.

So if your offer letter says ₹12 LPA CTC, your take-home could be anywhere from ₹75,000 to ₹85,000 per month, depending on your tax slab, investments declared, and deductions.

How to use your salary slip for financial planning

Here is how your salary slip connects to your bigger financial picture:

1. Maximise HRA exemption: If you pay rent, make sure you submit rent receipts to HR. This reduces your TDS significantly.

2. Submit investment proofs on time: Declare your 80C investments (ELSS, PPF, LIC) and health insurance premiums (80D) to HR each year. Missing this means extra TDS deduction.

3. Check your EPF balance: Your EPF is building up quietly every month. Check it on the EPFO portal (epfindia.gov.in) using your UAN number.

4. Understand your tax liability: Use your gross salary to estimate your annual income and figure out which tax slab you fall in.

5. Negotiate wisely: If you are switching jobs, understanding your salary structure helps you compare offers better — a higher CTC with a lower basic may mean less EPF, lower gratuity, and lower take-home than you expect.

The bottom line

Your salary slip is not just a receipt for your work. It is a financial document that affects your taxes, retirement savings, and take-home pay every single month. Understanding it takes 10 minutes — and that knowledge can save you thousands of rupees a year.