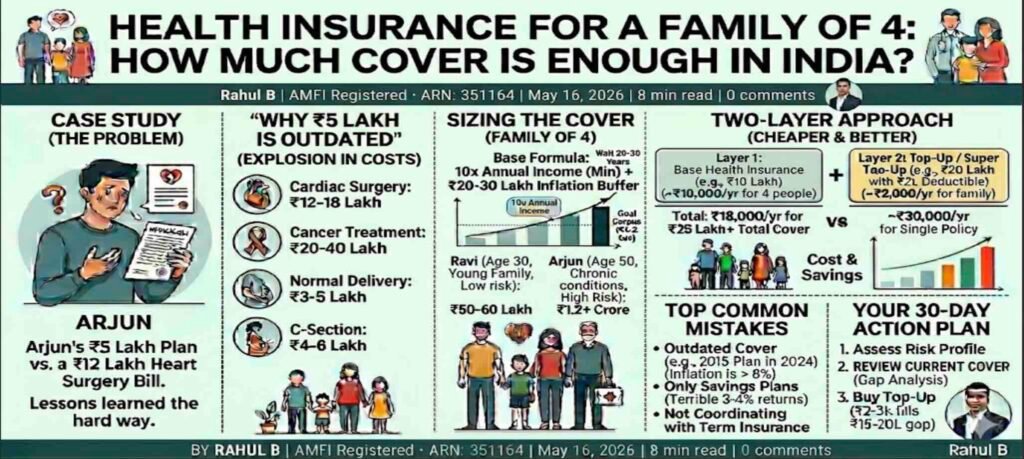

Arjun’s wife woke him up at 2 AM. “My chest feels tight.”

48 hours later, the hospital bill arrived: ₹12 lakhs for a heart surgery.

Arjun had health insurance. ₹5 lakh cover. The insurance paid ₹5 lakhs. Arjun paid ₹7 lakhs from his pocket. He borrowed ₹3 lakhs from his brother. Paid ₹4 lakhs from his savings. The family savings, built over 10 years, was gone in one surgery.

The worst part? He thought ₹5 lakh was enough. Everyone he knew had ₹5 lakh cover. His agent had recommended ₹5 lakh. So ₹5 lakh it was.

Two years later, he’d corrected the gap. But the damage was done. The lesson was learned the hard way: **₹5 lakh cover in 2024 is not enough for an Indian family of 4.**

This post will tell you exactly how much you need—and more importantly, why.

Why Health Insurance Sizing is Different in India

Health costs have exploded. In 2010, a good hospitalization cost ₹2-5 lakhs. Today, it’s ₹10-25 lakhs for serious procedures.

A cancer treatment? ₹20-50 lakhs.

A cardiac surgery? ₹10-15 lakhs.

A major accident? ₹15-30 lakhs.

Most Indians have a 10-year-old mental model of health costs. They buy ₹5 lakh cover and feel safe.

But they’re not. They’re just unaware of the gap.

Let me show you the actual costs.

Real Health Costs in India (2024)

| Procedure | Cost (Private Hospital) | Cost (Super Specialty) |

| Normal delivery | ₹1.5-3 lakh | ₹3-5 lakh |

| C-section | ₹2.5-4 lakh | ₹4-6 lakh |

| Appendectomy | ₹1.5-3 lakh | ₹3-5 lakh |

| Hernia surgery | ₹1-2 lakh | ₹2-3 lakh |

| Cataract surgery | ₹50k-1.5 lakh | ₹1.5-3 lakh |

| Knee replacement | ₹3-5 lakh | ₹5-8 lakh |

| Hysterectomy | ₹2-4 lakh | ₹4-6 lakh |

| Angiography + Stent | ₹3-5 lakh | ₹5-8 lakh |

| CABG (Bypass) | ₹8-12 lakh | ₹12-18 lakh |

| Cancer – Chemotherapy (6 months) | ₹10-20 lakh | ₹20-40 lakh |

| ICU stay (per day) | ₹10-20k | ₹20-50k |

One serious illness = ₹10-30 lakhs in a good private hospital.

If you have ₹5 lakh cover, you’re ₹5-25 lakhs short.

The Right Formula for Family Health Insurance

Here’s how to size health insurance for a family of 4:

Step 1: Assess Your Risk Profile

Age Profile:

– Younger family (all < 40): Lower risk

– Middle-aged (40-50): Moderate risk

– Senior members (60+): High risk

Health History:

– No serious illnesses: Low risk

– Diabetes, BP, etc.: Moderate risk

– Cancer history, multiple surgeries: High risk

Lifestyle:

– Sedentary, poor nutrition: Higher risk

– Active, healthy habits: Lower risk

Income Level:

– Lower income: Prefer government hospitals, less elaborate care

– Middle income: Mix of private and government

– High income: Always private, super specialty

Step 2: Base Cover Formula

Base formula: 10x your annual family income (minimum)

For a family earning ₹60 lakh/year (₹5 lakh/month):

– Base cover = ₹60 lakh

For a family earning ₹30 lakh/year (₹2.5 lakh/month):

– Base cover = ₹30 lakh

Why 10x? Because the most serious illnesses (cancer, major surgeries, long ICU stays) can exceed 15-20% of annual income. Adding buffer for multiple illnesses, you need 10x.

Step 3: Adjust for Risk

– **Low risk family**: Base × 0.7 (so 7x income)

– **Moderate risk family**: Base × 1.0 (10x income)

– **High risk family**: Base × 1.5 (15x income)

Step 4: Add Top-Up for Inflation

Health costs inflate at 8-10% annually (faster than general inflation). If you’re buying a 25-year policy, costs will triple.

Add **₹20-30 lakhs extra** to your base to account for inflation and cost escalation.

Real Examples: What Different Families Need

Family 1: Ravi (Age 30, Wife 28, Kids 5 & 2)

– Annual income: ₹50 lakh (₹4.1 lakh/month)

– Risk profile: Low (all healthy, young)

– Preferred hospitals: Good private

– Base cover needed: 50 lakh × 1.0 (moderate = assumes some risk over 20 years)

– **Recommended cover: ₹50-60 lakh**

Family 2: Arjun (Age 50, Wife 48, Both have BP)

– Annual income: ₹72 lakh (₹6 lakh/month)

– Risk profile: High (both have chronic conditions)

– Preferred hospitals: Super specialty

– Base cover needed: 72 lakh × 1.5 = ₹1.08 crore

– Add inflation buffer: +₹25 lakh

– **Recommended cover: ₹1.2+ crore**

Family 3: Priya (Age 60, Spouse 58, Both retired)

– Annual income: ₹20 lakh (₹1.67 lakh/month)

– Risk profile: High (age 60+)

– Preferred hospitals: Good private + government

– Base cover needed: 20 lakh × 1.5 = ₹30 lakh

– Add inflation buffer: +₹10 lakh

– **Recommended cover: ₹40 lakh minimum**

Family 4: Deepak (Self-employed, Wife, 1 Kid, Age 45)

– Annual income: Variable, average ₹40 lakh

– Risk profile: Moderate to High (self-employed, age 45)

– Preferred hospitals: Good private

– Base cover needed: 40 lakh × 1.2 = ₹48 lakh

– Add inflation + emergency buffer: +₹20 lakh

– **Recommended cover: ₹60+ lakh**

Two-Layer Approach (Best Strategy)

Most financial planners recommend a two-layer approach:

Layer 1: Base Health Insurance (₹5-10 lakh per person)

– Covers routine hospitalizations, surgeries

– Lower deductible

– Easier claims

– Cost: ₹3,000-5,000/person/year

Best options: HDFC ErgoGo, ICICI Lombard Active, Bajaj Allianz HealthGuard

Layer 2: Top-Up / Super Top-Up (₹10-20 lakh)

– Covers serious illnesses, major surgeries

– High deductible (₹1-2 lakh)

– Pays after base insurance is exhausted

– Cost: ₹1,500-3,000/year (very cheap)

How it works:

Cancer treatment = ₹20 lakhs

– Base insurance (₹10 lakh) covers ₹10 lakhs

– Top-up (₹15 lakh with ₹2 lakh deductible) covers remaining ₹8 lakhs

– Family pays: ₹2 lakhs (deductible)

– Total covered: ₹18 lakhs

Two-layer cost for a family of 4:

– Base: ₹4,000 × 4 = ₹16,000/year

– Top-up: ₹2,000 × 1 = ₹2,000/year (family-based)

– **Total: ₹18,000/year for ₹25 lakh+ total cover**

Compare this to:

– Single ₹25 lakh policy: ₹25,000-30,000/year

The two-layer approach is cheaper AND better.

What About Government Insurance (Ayushman Bharat)?

Ayushman Bharat gives ₹5 lakh cover to eligible families (income < certain limit).

Good for: People with low incomes, basic care

Not good for: Super specialty hospitals, choice of hospitals, no waiting

Our recommendation:

– If eligible AND low income: Use Ayushman Bharat as base + buy top-up private cover

– If eligible AND middle+ income: Buy private insurance (Ayushman Bharat limited network)

Common Mistakes in Health Insurance

Mistake 1: Buying Exactly What the Agent Recommends

Agents sell ₹5 lakh because it’s standard. It’s outdated. You need more.

Mistake 2: Not Reviewing Your Cover for 5-10 Years

You bought ₹5 lakh cover in 2015. It’s 2024. Health costs have doubled. You need to review and increase.

Mistake 3: Buying Only Savings Plans

“₹5 lakh cover + maturity benefit of ₹15 lakh” sounds good. But maturity benefits are poor returns (3-4%), and it increases your premium 5x.

Buy pure term health insurance. Invest separately.

Mistake 4: Not Coordinating with Term Insurance

You have ₹1 crore term insurance (death protection). But if you’re alive but seriously ill, you need health insurance. Both are necessary.

Mistake 5: Waiting Until You’re Old

At 60, a ₹15 lakh cover policy costs ₹20,000/year. At 40, the same cover costs ₹5,000/year. Buy health insurance while you’re young.

What to Actually Buy (Our Recommendation for Most Families)

For family earning ₹4-6 lakh/month:

Base Insurance (₹10 lakh per person):

– HDFC ErgoGo or ICICI Lombard Active

– ₹3,000-4,000/person/year

– For 4 people: ₹12,000-16,000/year

– Covers routine surgeries, hospitalizations

Top-Up Insurance (₹20 lakh):

– HDFC ErgoGo Top-Up or Max Bupa Super Top-Up

– ₹2,000-3,000/year for whole family

– Deductible: ₹1-2 lakh

– Covers major illnesses

Total annual cost: ₹15,000-20,000

Total cover: ₹40-50 lakh base + ₹20 lakh top-up = ₹60-70 lakh effective

Understanding Deductibles and No-Claim Bonuses

Deductible

The amount you pay before insurance starts paying.

Example: ₹1 lakh deductible, ₹20 lakh surgery

– You pay: ₹1 lakh

– Insurance pays: ₹19 lakh

Lower deductible = Higher premium

Higher deductible = Lower premium

For top-up insurance, higher deductible is fine because your base insurance already covers initial costs.

No-Claim Bonus

If you don’t claim, your cover increases annually.

Example: ₹10 lakh cover with 10% NCB annually

– Year 1: ₹10 lakh

– Year 2 (no claim): ₹11 lakh

– Year 3 (no claim): ₹12.1 lakh

This is valuable. Choose policies with good NCB.

The Planner Advantage

A financial planner does:

1. **Right-sizes your cover** based on income, age, risk, inflation

2. **Recommends base + top-up strategy** (optimal cost)

3. **Coordinates with other insurance** (ensures no gaps)

4. **Reviews annually** (checks if cover is still adequate)

5. **Helps with claims** (navigation when you need it most)

Most people buy insurance alone and hope for the best. Then when they need it, they discover gaps.

—

Your Action Plan (This Month)

1. **List all family members** and their ages

2. **Calculate your annual income**

3. **Assess your risk profile** (low/moderate/high)

4. **Calculate recommended cover** (10x income, adjusted for risk)

5. **Review your current cover** (check existing policies)

6. **Calculate the gap** (need – have)

7. **Get quotes for base + top-up** (don’t buy single high-value policy)

8. **Buy top-up** if you have gaps (costs ₹2-3k, fills ₹15-20 lakh gap)

This month, just get the coverage right. Next month, we’ll talk about claims and exclusions.

—

Key Takeaways

– **₹5 lakh cover is not enough for a family of 4 in 2024.** You need ₹40-60 lakh minimum.

– **Formula: 10x annual income + inflation buffer.** Adjust for age and risk.

– **Two-layer approach (base + top-up) is cheaper than single high-value policy.** Same cover, lower premium.

– **Review your cover every 2-3 years.** Health costs inflate faster than general inflation.

– **Buy pure health insurance, not savings plans.** Savings plans have terrible returns.

—

Disclaimer

This article is for educational purposes only. Your specific cover needs may differ based on personal circumstances, existing coverage, and geographic location. Consult a certified health insurance advisor before making changes.

Rahul Bhaskar | AMFI ARN: 351164 | [rahulmoney.com](https://rahulmoney.com)

*Need help sizing health insurance for your family? Let’s review your current cover together.*