Rekha stared at the confirmation screen on her phone.

SIP Registered Successfully Amount: ₹2,000/month Fund: HDFC Flexi Cap Fund Start Date: 1st of next month

Her thumb hovered over the “Done” button. One tap and it would be official. She’d be an investor.

But her brain was screaming objections:

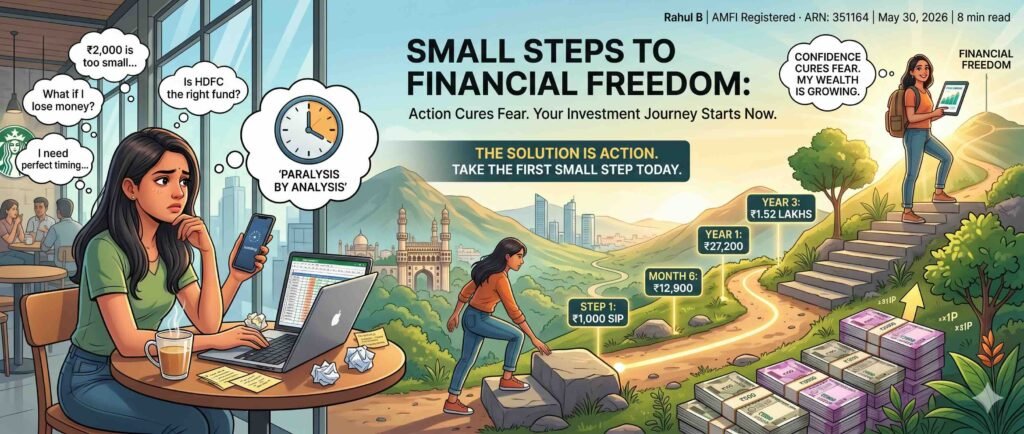

₹2,000 is nothing. What difference will it even make? What if I picked the wrong fund? What if the market crashes next month? What if I need this money for an emergency?

She closed the app without tapping “Done.”

Two weeks later, she was having chai with her friend Arjun.

“Did you start that SIP you were talking about?” he asked.

“Not yet,” Rekha said. “I’m still figuring it out.”

Arjun smiled. “You know what’s funny? I said the exact same thing for six months. Then I realized I wasn’t ‘figuring it out.’ I was just scared.”

“I’m not scared,” Rekha protested. “I’m being careful.”

“Being careful is doing research before you start,” Arjun said. “Being scared is researching forever and never starting.”

—

The Confidence Paradox

David Schwartz makes a bold claim in The Magic of Thinking Big:

“Action cures fear. Inaction feeds it.”

Most people get this backwards.

They think: Once I feel confident, I’ll take action.

But confidence doesn’t work like that. Confidence isn’t something you find. It’s something you build.

And you build it by doing the thing you’re afraid of—over and over—until it stops being scary.

When it comes to money, the pattern looks like this:

Beginner: Afraid to invest. Waits for the “right time.”

After First SIP: Still nervous, but less terrified. At least it’s done.

After 6 Months: Checks portfolio occasionally. Sees small gains (or losses). Realizes the world didn’t end.

After 1 Year: Increases SIP amount. Feels like an investor now.

After 3 Years: Advising friends on which funds to pick. Confidence is second nature.

Notice the sequence: Action → Experience → Confidence

Not: Confidence → Action.

You don’t wait to feel brave. You act, and bravery follows.

—

Why We Wait for “Perfect”

Rekha’s hesitation wasn’t unusual. Most people delay investing because they’re waiting for optimal conditions:

– The perfect fund – The perfect amount to start with – The perfect market entry point – The perfect level of knowledge

But here’s the problem: Perfect never arrives.

There will always be a “better” fund launched next month. The market will always be “too high” or “too volatile.” You’ll never feel like you’ve learned “enough.”

Waiting for perfect is just fear wearing a disguise.

Schwartz calls this “paralysis by analysis”—the illusion of progress through endless planning, while nothing actually gets done.

Rekha had read 12 articles on mutual funds. She’d compared expense ratios. She’d watched YouTube videos on SIP strategies.

But she still hadn’t invested a single rupee.

Knowledge without action is just trivia.

—

The Power of Starting Small

Arjun shared his story with Rekha.

“When I started, I invested ₹3,000 a month,” he said. “Not because it was optimal. Because it was what I could afford without panicking.”

“₹3,000 feels so small,” Rekha said. “Like it won’t even make a difference.”

“That’s what I thought too,” Arjun said. “But here’s what happened.”

He pulled out his phone and showed her his portfolio summary:

Year 1: ₹36,000 invested → ₹39,800 portfolio value (+₹3,800) Year 2: ₹72,000 invested → ₹89,200 portfolio value (+₹17,200) Year 3: ₹108,000 invested → ₹1,52,400 portfolio value (+₹44,400)

“By Year 3, I’d stepped up to ₹5,000/month,” Arjun explained. “But the point is: starting small didn’t hurt me. It saved me.”

“How?”

“Because if I’d waited until I could invest ₹10,000/month, I’d still be waiting. I would’ve lost three years of compounding.”

Rekha looked at the numbers again. ₹1.52 lakhs. From ₹3,000/month.

It wasn’t life-changing money. But it was real money. Money that wouldn’t exist if Arjun had kept researching instead of starting.

—

The First SIP: What Actually Happens

Schwartz writes: “Do what you fear, and fear disappears.”

Let’s walk through what actually happens when you start your first SIP—not the fantasy version, but the messy reality.

**Day 1: You Hit “Confirm”**

Heart racing. Second-guessing. Did I just make a huge mistake?

But also: a tiny spark of pride. I did it. I’m an investor now.

**Month 1: First Debit**

₹2,000 debits from your account. You barely notice. Life goes on.

**Month 2: You Check Your Portfolio**

Value: ₹4,100. You invested ₹4,000. You’re up ₹100!

You feel like a genius.

**Month 4: Market Dips**

Value: ₹7,800. You invested ₹8,000. You’re down ₹200.

Panic sets in. I knew this was a bad idea.

**Month 6: You Stop Checking Daily**

You realize obsessing over daily fluctuations is exhausting. You check once a month instead.

Value: ₹12,600. Invested: ₹12,000. Up ₹600.

Okay. This is fine.

**Month 12: First Milestone**

Value: ₹26,800. Invested: ₹24,000. Up ₹2,800.

You increase your SIP to ₹3,000/month. It feels… easy now.

**Month 18: Confidence Kicks In**

A colleague asks you about mutual funds. You find yourself explaining SIPs, CAGR, and expense ratios.

Wait. When did you become the person who knows this stuff?

—

Rekha’s First Step

After that conversation, Rekha made a decision.

She wouldn’t wait for perfect. She’d start with possible.

She opened her banking app and set up a ₹2,000/month SIP in the same fund Arjun used. Not because it was the best fund in the universe, but because it was good enough and Arjun’s results proved it worked.

The confirmation screen appeared again.

This time, she tapped “Done.”

Her heart was still racing. Her brain was still whispering doubts. But she’d done it.

She was an investor.

—

What Happened Next (Spoiler: Not Disaster)

Month 1: Rekha checked her portfolio five times a day. Value: ₹2,040. She’d made ₹40!

Month 3: Market corrected. Value: ₹5,850. Invested: ₹6,000. She was down ₹150.

She texted Arjun in a panic: “Should I stop the SIP?”

He replied: “Remember what I told you. This is when you buy cheap. Don’t stop now.”

She didn’t stop.

Month 6: Value: ₹12,900. Invested: ₹12,000. Up ₹900.

The fear was fading.

Month 12: Value: ₹27,200. Invested: ₹24,000. Up ₹3,200.

She increased her SIP to ₹3,500/month.

Month 18: Value: ₹50,800. Invested: ₹45,000. Up ₹5,800.

Her cousin asked her about investing. Rekha found herself explaining SIPs, rupee cost averaging, and why market dips are buying opportunities.

She sounded exactly like Arjun had 18 months ago.

—

The Three Confidence Builders

Schwartz identifies three ways action builds confidence:

1. **Proof of Capability**

Before starting, Rekha thought: I’m not the kind of person who invests.

After six months, she thought: I’m literally an investor. The proof is in my portfolio.

Identity shifted. Not through affirmations or vision boards. Through action.

2. **Diminishing Fear Through Repetition**

Month 1: Terrified. Month 3: Nervous. Month 6: Cautious. Month 12: Comfortable. Month 18: Confident.

The SIP debit that once felt like a leap of faith now felt like brushing her teeth. Automatic. Normal.

3. **Competence Through Experience**

Rekha didn’t learn about investing by reading articles forever.

She learned by: – Starting a SIP – Watching it grow (and dip) – Making mistakes (checking too often, panicking during corrections) – Adjusting (stopping the daily checks, trusting the process) – Seeing results (₹5,800 in gains)

Experience taught her what theory never could: I can handle this.

—

Start Small, But Start *Now*

Here’s the most important lesson Schwartz teaches:

Small, imperfect action beats perfect inaction every single time.

Rekha’s ₹2,000/month wasn’t optimal. If she’d started with ₹5,000, she’d have more money today.

But if she’d waited until she could “afford” ₹5,000, she’d have ₹0 today.

₹27,200 beats ₹0.

Arjun’s ₹3,000/month wasn’t ideal. But it was infinitely better than waiting.

Your first SIP doesn’t need to be perfect. It needs to be started.

—

The Five-Minute Confidence Builder

If you’re scared to start investing, here’s Schwartz’s prescription:

**Step 1: Commit to One Small Action (5 Minutes)**

Don’t commit to “becoming an investor” or “building a ₹1 crore portfolio.”

Commit to: I will set up a ₹1,000/month SIP this week.

That’s it.

**Step 2: Take the Action Before You “Feel Ready”**

You’ll never feel ready. Do it scared.

Open your banking app. Pick any decent flexi-cap or index fund. Set up ₹1,000/month. Hit confirm.

**Step 3: Don’t Check It for 30 Days**

Seriously. Don’t obsess. Let it run.

Checking daily just feeds fear. Letting it run builds confidence.

**Step 4: After 30 Days, Notice What Happened**

Probably nothing dramatic. Maybe you’re up ₹50. Maybe down ₹30.

But here’s what definitely happened: You didn’t die. The world didn’t end. You’re still fine.

And now you have proof: I can do this.

**Step 5: Increase the Amount (When Ready)**

Once you’re comfortable with ₹1,000, bump it to ₹2,000.

Then ₹3,000.

Then ₹5,000.

Each step builds confidence for the next.

—

The Transformation: From Scared to Steady

Two years after starting her first ₹2,000 SIP, Rekha was investing ₹8,000/month across three funds.

Her portfolio: ₹2.4 lakhs.

But the real change wasn’t the money.

It was how she felt.

She no longer waited for permission to make financial decisions. She didn’t need Arjun’s approval to pick a fund. She didn’t panic when the market dropped 10%.

She’d gone from someone who was afraid of investing to someone who was confident in her ability to build wealth.

Not because she’d become a financial genius.

But because she’d taken one small, scared, imperfect action—and then another, and another.

Confidence didn’t come from knowledge. It came from doing.

—

Next in the series: The ₹1 Crore Question: Why Thinking Small Keeps Your Bank Account Small

—

Disclaimer: This article is for educational purposes only. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. The author is a SEBI-registered Mutual Fund Distributor (ARN 351164). Past performance is not indicative of future returns.