Rajesh made a decision that cost his family ₹50 lakhs.

At 35, he’d walked into an LIC office and bought a traditional endowment plan. It sounded good: “₹1 lakh premium every year for 20 years. Get ₹30 lakh maturity + bonuses. Plus, if you die, your family gets ₹30 lakh.”

He felt safe. Protected. Smart.

25 years later (he’s now 60), he’s done the math. Over 25 years, he paid ₹25 lakh in premiums. He got ₹32 lakh back. **Net profit: ₹7 lakh. That’s 2.8% annual return.**

Meanwhile, a colleague bought term insurance. He paid ₹15,000/year for a ₹1 crore cover. At 60, he’d paid ₹3.75 lakh in premiums and his family had ₹1 crore protection.

The same ₹3.75 lakh invested in a mutual fund SIP? It would’ve grown to ₹40 lakhs at 12% returns.

The difference in final wealth: ₹45 lakhs.

That’s the story of term insurance vs. LIC plans in India. Not straightforward, but crucial.

Why This Confusion Exists

LIC has been in India for 60 years. Your father bought an LIC plan. Your uncle bought an LIC plan. It’s like oxygen—everyone assumes it’s good.

But good for what?

– **Good savings vehicle?** Terrible (2-3% returns)

– **Good protection?** Expensive (costs 10x more per rupee of cover)

– **Good investment?** Risky (linked to market, poor transparency)

Term insurance, on the other hand, is boring. No maturity benefits. No bonuses. Just: “If I die, my family gets money.”

Nobody’s excited about boring. But boring is often the right choice in finance.

Let’s break this down with numbers.

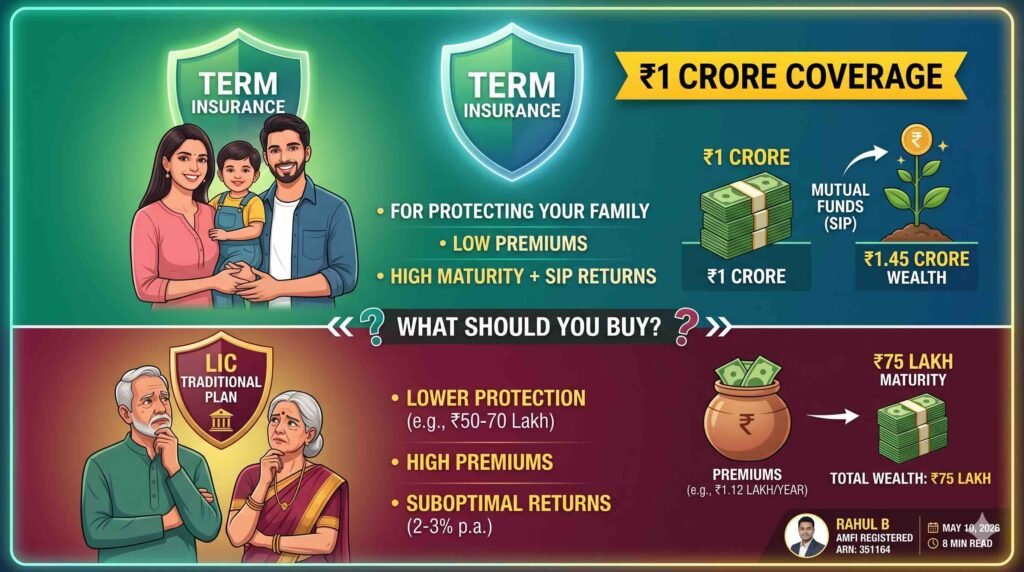

The Scenario: Protecting a ₹1 Crore Family Need

You’re 30 years old. You have a wife, 2 kids, and a home loan. You want ₹1 crore protection.

Option 1: LIC Traditional Endowment Plan

– Premium: ₹80,000/year (₹6,666/month)

– Duration: 20 years

– Sum Assured: ₹50 lakh

– Maturity Benefit: ₹50 lakh + bonuses (~₹15-20 lakh)

– Death Benefit: ₹65-70 lakh

– Total Paid: ₹16 lakh over 20 years

– Problem: Only ₹70 lakh cover, not ₹1 crore. Need 1.4 policies.

Real cost for ₹1 crore cover: ₹1.12 lakh/year

Option 2: Term Insurance

– Premium: ₹20,000/year (₹1,666/month)

– Duration: 30 years (to age 60)

– Sum Assured: ₹1 crore

– Death Benefit: ₹1 crore (no matter when you die)

– Maturity Benefit: ₹0 (unless you live past 60, then some plans return premiums)

– Total Paid: ₹6 lakh over 30 years

Total paid for ₹1 crore cover: ₹6 lakh

The Financial Comparison

Let’s track what happens over 30 years:

Scenario A: You Live Till 60

LIC Plan | Term Insurance | |

Total premiums paid (30 years) | ₹16.8 lakh (for ₹1 crore) | ₹6 lakh |

Maturity/Survival Benefit | ₹75 lakh (LIC endowment) | ₹0 |

Net cost of protection | ₹16.8 – ₹75 = -₹58.2 lakh | ₹6 lakh |

**Effective return** | **2.8% p.a.** | **N/A (pure protection)** |

Wait, this looks like LIC is better? Negative cost?

Not if you invest the premium difference:

LIC | Term + SIP (Difference) | |

Premium paid | ₹1.12 lakh/year | ₹20,000/year |

Difference | – | ₹92,000/year |

Invest the difference at 12% p.a. | – | **₹1.45 crore at age 60** |

LIC maturity + bonuses | ₹75 lakh | – |

**Total wealth at 60** | **₹75 lakh** | **₹1.45 crore** |

**Difference** | **₹70 lakh more with term** |

Scenario B: You Die at 45 (God forbid)

LIC Plan | Term Insurance | |

Death benefit received | ₹70 lakh | ₹1 crore |

Premiums paid so far | ₹10.8 lakh | ₹3 lakh |

**Net received** | **₹59.2 lakh** | **₹97 lakh** |

Your family needs ₹1 crore to cover the home loan, living expenses, and children’s education. LIC pays ₹70 lakh. Your family is ₹30 lakh short. Term pays ₹1 crore. Problem solved.

Why is Term Insurance So Much Cheaper?

Term insurance is simple: You pay a premium. If you die in the term, we pay. If you don’t die, we keep it. No bonuses, no maturity, no complexity.

LIC plans are bundled: Insurance + savings + investment + bonuses + legacy management + agent commission (20-40% of first year premium).

All that bundling costs money. **You’re paying for features you don’t want.**

It’s like buying a car with an advanced sound system when you can’t hear. You’re paying ₹50,000 extra for something you don’t use.

But Wait—My Agent Said…

Let me address the common objections:

Objection 1: “Term gives nothing if you survive”

Truth: You don’t buy insurance for yourself. You buy it for your family. If you die, they need money. If you survive, you’ve already transferred that risk from your family to an insurance company. That’s a win.

You buy a seatbelt to protect you if you crash. If you never crash, you don’t get the seatbelt money back. You just survived.

Objection 2: “LIC is safer than term insurance companies”

Truth: All insurance companies are regulated by IRDAI. They have minimum solvency ratios. If an insurance company fails, your claims are paid from the industry insurance fund. Size doesn’t matter; regulation does.

LIC is no safer than HDFC Life or Max Life. It’s just older.

Objection 3: “Term premiums increase every year”

Truth: Level term premiums don’t increase. Once you buy a 30-year term policy, your premium is locked at ₹20,000/year for all 30 years. Some companies offer “renewable term” where premiums go up after 10 years, but level term is standard now.

Objection 4: “I want both protection and savings”

Truth: So do I. But do it separately.

Buy term insurance for protection. Invest the difference in a mutual fund SIP. At 45, you’ll have ₹40 lakhs in mutual funds + ₹1 crore protection. At 60, you’ll have ₹1.45 crore + still have the cover (though you might reduce it).

When you bundle savings + insurance, you get suboptimal returns on both.

The Only Scenario Where LIC Plans Make Sense

There’s one scenario: **You have no discipline to invest the difference.**

If buying an LIC plan forces you to save ₹1.12 lakh/year (because of the premium), and you’d otherwise spend it, then LIC is better than nothing.

But honestly? That’s poor financial planning. It’s like saying, “I need handcuffs to stop myself from eating ice cream.”

The real solution is **automating your SIP**. Set it and forget it.

What Term Insurance Should You Buy?

If you decide on term (which I recommend), here’s the framework:

How Much Cover?

Use this formula:

Cover = (Home loan balance) + (10 × Annual living expenses) + (5 × Children’s education cost)

Example for Ravi:

– Home loan balance: ₹30 lakh

– Annual living expenses: ₹10 lakh (so 10 years = ₹1 crore)

– Children’s education: ₹10 lakh per kid × 2 kids = ₹20 lakh

– **Total cover needed: ₹1.5 crore**

How Long?

Until your children are independent and your home loan is paid off. Usually 25-30 years.

How Much Premium?

For Ravi (age 30, non-smoker, ₹1.5 crore cover, 30-year term):

– HDFC Life SmartClick: ₹1,500/month

– Max Life Online Term: ₹1,400/month

– ICICI Pru Click2Protect: ₹1,450/month

All are roughly ₹15,000-20,000/year for ₹1 crore cover.

Which Company?

HDFC Life, Max Life, ICICI Prudential, Bajaj Life, SBI Life are all safe and regulated. Pick based on:

– Premium cost

– Claim settlement ratio (check IRDAI reports)

– Ease of online management

Don’t pick based on advertising. Don’t let an agent pressure you. Just pick one, buy online, done.

The Hybrid Approach (If You Want Both)

If you absolutely must have savings + insurance, here’s the optimal way:

1. **Buy term insurance for your protection** (₹20,000/year)

2. **Buy a small LIC/ULI endowment plan** (₹20,000/year) for forced savings (only if you lack discipline)

3. **Invest the rest in mutual funds** (₹50,000/year)

This gives you:

– ₹1 crore protection at low cost

– Forced savings discipline

– Market-linked growth

– Flexibility to pause investments if needed

But honestly? Most people are better off with just term + mutual fund SIP.

Real Life: What Happened to Rajesh and His Colleague

Rajesh (LIC plan):

– Paid ₹25 lakhs over 25 years

– Got ₹32 lakhs maturity benefit

– Family had ₹30 lakh protection (not enough today)

– Real return: 2.8% p.a.

His colleague (term + SIP):

– Paid ₹3.75 lakhs in term premiums over 25 years

– Built ₹40 lakhs in mutual fund SIPs

– Family had ₹1 crore protection all 25 years

– Real return: 12% p.a.

At 60, his colleague has ₹1.45 crore. Rajesh has ₹32 lakhs. The difference in life quality? Significant.

The Planner Advantage

Here’s what a financial planner does:

1. **Right-sizes your cover** (not too much, not too little)

2. **Chooses the right type** (term for most, endowment only if discipline is low)

3. **Recommends the right company** (highest claim settlement, lowest premium)

4. **Coordinates with other insurance** (health + life + term all together)

5. **Reviews it annually** (adjusts cover as life changes)

Most people leave this to agents who earn commissions on LIC plans. That’s like asking a Hyundai dealer if you should buy a Hyundai.

—

Your Action Plan (This Month)

1. **Calculate your insurance need** (home loan + 10 years expenses + kids’ education)

2. **Check your current cover** (if you have an LIC plan, note what it gives)

3. **Compare the gap** (need ₹1 crore, have ₹30 lakh? Gap is ₹70 lakh)

4. **Get term quotes** (HDFC, Max, ICICI online)

5. **Stop meeting LIC agents** (until you decide on a plan)

6. **Buy term online** (within 1 week)

If you have existing LIC plans, don’t surrender them (tax implications). Just add term insurance on top.

—

Key Takeaways

– **Term insurance gives ₹1 crore protection for ₹20,000/year. LIC endowment gives ₹70 lakh for ₹1.12 lakh/year.** The math is clear.

– **Insurance is not an investment.** Stop expecting maturity benefits. Buy term for protection, invest separately for wealth.

– **The premium difference invested in mutual funds creates ₹70 lakhs more wealth** over 30 years.

– **LIC plans make sense only if you lack discipline to invest on your own.** Even then, it’s not optimal.

– **All insurance companies are safe.** Regulation and claim settlement matter, not age.

—

Disclaimer

This article is for educational purposes. The views on LIC vs. term insurance are based on financial returns analysis, not a criticism of LIC as an institution. Your situation may differ based on personal goals, income, and tax situation. Consult a certified financial planner before making changes to insurance.

Rahul Bhaskar | AMFI ARN: 351164 | [rahulmoney.com](https://rahulmoney.com)

*Confused about your insurance? Let’s simplify it together.*