Ravi was filling out a financial planning questionnaire at his new bank.

“What is your 10-year financial goal?”

He paused. His pen hovered over the blank line.

What’s a reasonable goal? he thought.

He did some mental math. He was 28. He earned ₹65,000/month. After expenses, he saved about ₹8,000. In 10 years, that would be ₹9.6 lakhs.

He wrote: “Save ₹10 lakhs in 10 years.”

It felt achievable. Safe. Realistic.

His friend Arjun, sitting next to him (they were opening accounts together), glanced over.

“₹10 lakhs? That’s it?”

Ravi frowned. “What do you mean ‘that’s it’? Ten lakhs is a lot of money.”

“It is,” Arjun said. “But is it enough?”

“Enough for what?”

“For anything,” Arjun said. “A car costs ₹12 lakhs. A flat down payment is ₹25 lakhs. Retirement needs at least ₹2 crores. What’s ₹10 lakhs going to do for you in 10 years?”

Ravi stared at his answer. Suddenly, “realistic” felt like another word for “small.”

—

The Problem with “Realistic” Goals

David Schwartz writes in The Magic of Thinking Big:

“Set goals that make you stretch. Big goals pull you forward. Small goals keep you stuck.”

Here’s the uncomfortable truth about small goals:

They feel safe. They feel achievable. But they also trap you in mediocrity.

Ravi’s ₹10 lakh goal wasn’t wrong. But it was small thinking disguised as prudence.

Why?

1. It doesn’t account for inflation. ₹10 lakhs in 10 years will buy what ₹6 lakhs buys today (at 5% inflation).

2. It doesn’t account for life goals. Want a house? ₹10 lakhs won’t cut it. Want to retire early? Not happening.

3. It doesn’t challenge growth. If ₹10 lakhs is your target, you’ll find ways to save ₹8,000/month and call it a day. You won’t push for raises, side income, or higher investments.

Small goals create small actions. Small actions create small results.

—

What “Thinking Big” Actually Means

Arjun pulled out his phone and opened a SIP calculator.

“Let me show you something,” he said.

He entered: – Monthly SIP: ₹10,000 – Time Period: 10 years – Expected Return: 12% CAGR

Result: ₹23.23 lakhs

Then he adjusted: – Monthly SIP: ₹10,000 (stepped up by 10% every year) – Time Period: 10 years – Expected Return: 12% CAGR

Result: ₹32.97 lakhs

“That’s almost ₹33 lakhs,” Arjun said. “From ₹10,000 a month. Not ₹8,000 in a savings account.”

Ravi stared at the numbers. “But I can’t invest ₹10,000 right now.”

“Not yet,” Arjun said. “But what if that became your goal? What would you need to change to make it possible?”

Ravi thought about it.

He’d need to: – Cut unnecessary expenses (eating out less, canceling unused subscriptions) – Ask for a raise (he’d been avoiding that conversation for a year) – Maybe pick up freelance work on weekends

None of it was impossible. It was just… bigger than he’d been thinking.

“What did you write?” Ravi asked, pointing at Arjun’s form.

Arjun flipped his paper around.

“Build a ₹50 lakh corpus in 10 years.”

Ravi laughed. “₹50 lakhs? On your salary?”

“Why not?” Arjun said. “If I step up my SIP every year, switch jobs once or twice for better pay, and stay consistent, the math works.”

“But what if you don’t hit it?”

“Then I’ll have ₹40 lakhs,” Arjun shrugged. “Still better than ₹10.”

—

Big Goals Force Better Questions

Schwartz makes a critical observation:

“Small thinking breeds small questions. Big thinking breeds breakthrough questions.”

When Ravi set a ₹10 lakh goal, his questions were: – “How do I save ₹8,000 this month?” – “Should I cut my Swiggy budget?” – “Is ₹10 lakhs enough for an emergency fund?”

When Arjun set a ₹50 lakh goal, his questions were: – “How can I double my income in 5 years?” – “What skills do I need to earn ₹1.5 lakhs/month?” – “Where should I invest to maximize returns safely?”

See the difference?

Small goals lead to optimization questions (How do I squeeze out ₹500 more?).

Big goals lead to transformation questions (How do I 2x my earning potential?).

—

The Four Levels of Financial Thinking

Let’s break down the spectrum from small thinking to big thinking in money terms:

**Level 1: Survival Thinking** (₹0-2 lakhs saved)

“I just want to get through this month without running out of money.”

This isn’t thinking. It’s firefighting. Every month is a scramble. No goals, no plan, just survival.

**Level 2: Small Thinking** (₹2-10 lakhs saved over 5-10 years)

“I’ll save whatever’s left at the end of the month and hope it’s enough.”

This is where most people live. They’re saving, but without a compelling target. Goals are vague: “build an emergency fund,” “save for a car someday.”

The problem? Small thinking doesn’t create urgency. There’s no forcing mechanism to push for more.

**Level 3: Medium Thinking** (₹20-50 lakhs in 10-15 years)

“I’ll invest regularly, track my portfolio, and aim for a specific target.”

This is where wealth-building begins. Goals are clear: “₹30 lakhs in 12 years for a house down payment.” Plans are concrete: “₹15,000/month SIP, step up by 10% annually.”

Medium thinkers take money seriously. They read, they plan, they adjust.

**Level 4: Big Thinking** (₹1 crore+ in 15-20 years)

“I’ll build wealth that gives me freedom—freedom to retire early, start a business, or never worry about money again.”

Big thinkers don’t just save. They build systems: – Multiple income streams (salary + freelance + investments) – Aggressive investing (₹20,000-50,000/month SIPs) – Strategic career moves (switching companies every 2-3 years for 30-50% raises) – Tax optimization (80C, 80D, NPS, ELSS)

Big thinking isn’t reckless. It’s ambitious and disciplined.

—

Ravi’s Shift: From ₹10 Lakhs to ₹40 Lakhs

After that conversation, Ravi went home and couldn’t stop thinking about Arjun’s ₹50 lakh goal.

Is that even possible for someone like me?

He opened a spreadsheet and started running numbers.

Current Situation: – Salary: ₹65,000/month – Monthly savings: ₹8,000 – 10-year goal (old): ₹10 lakhs

What If I Thought Bigger?

He plugged numbers into a SIP calculator:

Scenario 1: Stay Safe – ₹8,000/month in savings account – 10 years – 4% interest – Result: ₹11.8 lakhs

Scenario 2: Start Investing – ₹8,000/month SIP – 10 years – 12% CAGR – Result: ₹18.6 lakhs

Scenario 3: Think Bigger – ₹12,000/month SIP (cut expenses + earn more) – Step up by 10% annually – 10 years – 12% CAGR – Result: ₹39.5 lakhs

₹39.5 lakhs.

Ravi stared at the number. It felt impossible. But the math didn’t lie.

If he could increase his savings from ₹8,000 to ₹12,000 (by cutting ₹2,000 in expenses and earning ₹2,000 more somehow), and stepped it up every year, he’d have ₹40 lakhs in 10 years.

Not ₹10 lakhs. ₹40 lakhs.

The goal shifted from “realistic” to “challenging but possible.”

And that shift changed everything.

—

What Changed When Ravi Thought Bigger

**Month 1: New Goal Set**

Ravi rewrote his financial goal: “Build ₹40 lakhs in 10 years.”

It scared him. But it also excited him.

**Month 2: First SIP Started**

He couldn’t afford ₹12,000/month yet, so he started with ₹8,000. But now, instead of feeling like “this is all I can do,” it felt like “this is my starting point.”

**Month 4: Asked for a Raise**

Ravi had been putting off the conversation with his manager for over a year. The new goal gave him a reason to act.

He prepared a document outlining his contributions, took on extra responsibility, and asked for a 15% raise.

He got 12%. His salary went from ₹65,000 to ₹72,800.

**Month 6: Cut the Fat**

Ravi tracked his expenses obsessively for one month. He found: – ₹2,400/month on food delivery (cut to ₹1,000 by meal-prepping on Sundays) – ₹1,500/month on subscriptions he barely used (canceled all but one) – ₹3,000/month on “miscellaneous” impulse buys (set a strict budget)

Freed up: ₹5,000/month.

He increased his SIP from ₹8,000 to ₹11,000.

**Year 1: Side Hustle Unlocked**

Ravi was a graphic designer. He started taking freelance projects on weekends—₹3,000 here, ₹5,000 there. Some months he made ₹8,000 extra. Some months, nothing.

But over the year, freelancing brought in ₹48,000.

He didn’t spend it. He dumped it into his SIP as lump sums.

**Year 2: SIP Stepped Up**

After his annual raise (8%), Ravi increased his SIP to ₹13,500/month.

His portfolio: ₹3.2 lakhs (₹2.76 lakhs invested + ₹44,000 gains).

He was ahead of schedule.

—

Big Thinking Creates Big Opportunities

Here’s what Schwartz observed:

“Big goals magnetize resources. Small goals repel them.”

When Ravi had a ₹10 lakh goal, he thought: I just need to save a little more.

When he set a ₹40 lakh goal, he thought: I need to transform how I earn, save, and invest.

The ₹40 lakh goal didn’t just sit there passively. It pulled him forward.

It forced him to: – Have uncomfortable conversations (asking for a raise) – Build new skills (freelancing, investing knowledge) – Make sacrifices (meal-prepping, canceling subscriptions) – Take risks (switching jobs in Year 3 for a 30% salary jump)

Would he have done any of that for ₹10 lakhs? Probably not.

The big goal created urgency. And urgency creates action.

—

The ₹1 Crore Question

Five years into his journey, Ravi’s portfolio had crossed ₹12 lakhs.

He was on track for ₹40 lakhs in 10 years—maybe even ₹45 lakhs if the market stayed strong.

One day, Arjun asked him: “What’s your next goal?”

Ravi didn’t hesitate. “₹1 crore.”

Arjun grinned. “Now you’re thinking big.”

“You know what’s crazy?” Ravi said. “Five years ago, ₹1 crore felt like a fantasy. Something only rich people hit. Now it feels… inevitable. Like it’s just a matter of time and discipline.”

“That’s what big thinking does,” Arjun said. “It doesn’t make you delusional. It makes you capable.”

—

How to Set a Big Goal (Without Freaking Out)

If you’re stuck in small thinking, here’s how to shift:

**Step 1: Ask “What Would Be Amazing?”**

Forget “realistic” for a moment. Ask:

What would be an amazing financial outcome in 10 years?

₹50 lakhs? ₹1 crore? ₹2 crores?

Write it down. Don’t edit. Don’t rationalize. Just dream.

**Step 2: Reverse-Engineer the Math**

Plug your “amazing” goal into a SIP calculator. Work backwards.

Want ₹1 crore in 20 years? You need ₹15,000/month at 12% CAGR.

Suddenly, “impossible” has a price tag. And price tags are negotiable.

**Step 3: Break It into Milestones**

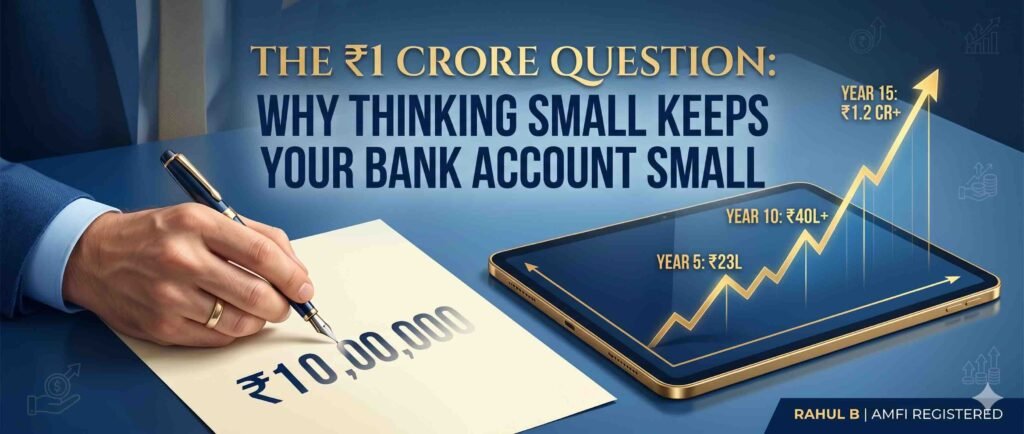

₹1 crore feels overwhelming. ₹10 lakhs in Year 5 feels doable.

Break the big goal into 5-year chunks: – Year 5: ₹10 lakhs – Year 10: ₹35 lakhs – Year 15: ₹75 lakhs – Year 20: ₹1.2 crores

Each milestone is a mini-goal. Achievable. Measurable.

**Step 4: Identify the Gap**

Where are you now? Where do you need to be?

If you’re saving ₹5,000/month and you need ₹15,000/month, the gap is ₹10,000.

Now ask: How do I close that gap?

Earn more? Cut expenses? Both?

**Step 5: Commit Publicly**

Tell someone your big goal. A friend. A spouse. A mentor.

Public commitment creates accountability. And accountability kills excuses.

—

Why Big Thinking Isn’t Reckless

Some people hear “think big” and assume it means:

– Taking stupid risks – Investing in shady schemes promising 50% returns – Quitting your job to become a day trader

That’s not big thinking. That’s gambling.

Big thinking is: – Setting an ambitious target (₹1 crore) – Using proven methods (SIPs, diversified mutual funds, compounding) – Staying disciplined (monthly investments, annual step-ups) – Playing the long game (15-20 years)

Big thinking is bold, not reckless.

—

Next in the series: “I Can’t Afford to Save”: The Creative Solution That Changed Everything

—

Disclaimer: This article is for educational purposes only. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. The author is a SEBI-registered Mutual Fund Distributor (ARN 351164). Past performance is not indicative of future returns.