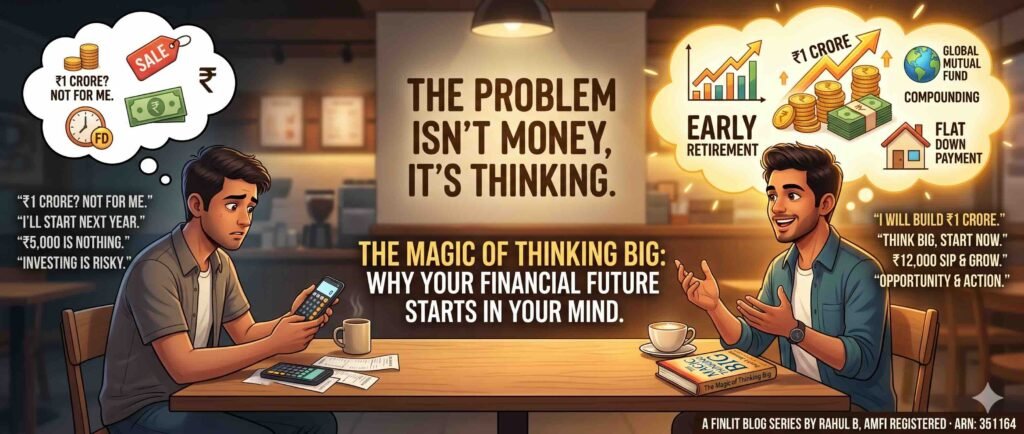

Ravi sat across from his college friend Arjun at a Starbucks in Banjara Hills, listening to something that sounded completely insane.

“I’m going to build a ₹1 crore corpus in the next 15 years,” Arjun said, stirring his cappuccino with the confidence of someone who’d just discovered fire.

Ravi blinked. “You make ₹60,000 a month. After rent, EMIs, and living expenses, you’re probably left with what—₹8,000? Maybe ₹10,000 on a good month?”

“₹12,000, actually. I’ve been tracking.”

“Okay, ₹12,000. That’s ₹1.44 lakhs a year. Even if you save every rupee for 15 years, that’s only ₹21.6 lakhs. Where’s this magical ₹1 crore coming from? A lottery ticket?”

Arjun smiled. “Equity mutual funds. SIPs. Compounding. And something else—a shift in how I think about money.”

Ravi raised an eyebrow. “Since when did you become a motivational speaker?”

“Since I read this book.” Arjun pulled out a worn paperback from his bag: The Magic of Thinking Big by David J. Schwartz.

Ravi glanced at the cover—outdated font, cheesy subtitle, the kind of self-help book his dad’s generation swore by. “A book from 1959 is going to make you a crorepati?”

“Not the book,” Arjun said. “The way I think after reading it.”

—

The Problem We Don’t See

Most of us don’t have a money problem. We have a thinking problem.

We think: – “₹1 crore is for people with high salaries, not me.” – “Investing is risky. I’ll wait until I have more saved up.” – “SIPs are good, but ₹5,000 a month won’t make a real difference.” – “I’ll start once I get that promotion. Or after my wedding. Or when my loans are done.”

These aren’t facts. They’re beliefs. And beliefs, as David Schwartz argues in The Magic of Thinking Big, are the invisible ceiling on our financial lives.

The book isn’t about money. It was written in 1959 for salespeople, managers, and professionals trying to climb the corporate ladder. But its core insight is universal and timeless:

Your success—in any area of life—is determined by the size of your thinking.

Think small, and you’ll find a hundred reasons why ₹1 crore is impossible. Think big, and you’ll find one way to make it happen.

—

What This Book Teaches (And Why It Matters for Money)

The Magic of Thinking Big is built on a simple, powerful premise: most people fail not because they lack ability, but because they think too small about what’s possible.

Schwartz identified patterns that separate high achievers from everyone else: – They believe success is possible before they have proof. – They eliminate excuses (what he calls “excusitis”) that justify inaction. – They take action despite fear, knowing confidence comes from doing, not waiting. – They set big goalsand reverse-engineer the steps. – They manage their environment—surrounding themselves with people who think bigger, not smaller.

Now, apply this to money.

What if the reason you’re stuck at ₹50,000 in savings isn’t because you don’t earn enough—but because you’ve convinced yourself that ₹50,000 is “good enough”?

What if the reason you haven’t started investing isn’t because the market is risky—but because thinking about risk feels safer than taking action?

What if your financial future isn’t limited by your salary, but by how big you’re willing to think?

—

The Ravi Test: Small Thinking vs. Big Thinking

Let’s go back to Ravi.

Ravi earns ₹65,000 a month. After expenses, he saves about ₹8,000. He keeps it in his savings account because “it’s safe.” Over five years, he’s accumulated ₹4.8 lakhs (ignoring interest, which is negligible).

He wants to buy a car worth ₹12 lakhs. At his current rate, it’ll take him 15 years to save enough. So he’s considering a loan.

Now meet Arjun.

Arjun earns ₹60,000 a month. After expenses, he invests ₹12,000 in equity mutual funds via SIP. Over five years, assuming a conservative 12% CAGR, his ₹7.2 lakhs in contributions grow to approximately ₹9.8 lakhs.

But here’s the kicker: Arjun doesn’t want a ₹12 lakh car. He’s thinking about a ₹40 lakh down payment on a flat. And he’s on track.

What’s the difference between Ravi and Arjun?

Not their salaries. Not their expenses. Not even their financial knowledge.

The difference is the size of their thinking.

Ravi thinks: “I’ll save what I can and hope it’s enough.”

Arjun thinks: “I’ll set a big goal and figure out how to reach it.”

—

Why We Think Small About Money

Schwartz identified four main reasons people think small. Let’s translate them to personal finance:

1. Excusitis (Making Excuses)

– “I don’t earn enough to invest.” – “The market is too risky right now.” – “I’ll start once I clear my loans.” – “Mutual funds are complicated. I’ll do it later.”

Every excuse is a ceiling. And ceilings feel safe—until you realize you’ve been living in a box.

2. Fear of Failure

Starting a SIP feels scary because what if the market crashes? What if you pick the wrong fund? What if you need that money in an emergency?

But here’s the truth: not investing is the biggest risk of all. Inflation silently erodes your savings account. Ten years from now, your ₹5 lakhs will buy what ₹3 lakhs buys today.

3. Lack of Belief

You’ve never seen ₹1 crore in your bank account, so your brain files it under “impossible.” You think it’s for people with ₹2 lakh salaries or family wealth, not for you.

But compounding doesn’t care about your current net worth. It cares about consistency and time.

4. Environmental Conditioning

Your friends say, “Mutual funds? Just do an FD, man. Guaranteed returns.” Your parents say, “Invest in gold, beta. It’s safe.” Your colleagues say, “I tried SIPs once. Lost money. Never again.”

You absorb these voices. And slowly, without realizing it, you start thinking their thoughts instead of your own.

—

The Transformation Arjun Made (And You Can Too)

When Arjun first read The Magic of Thinking Big, he was stuck in the same mental traps as Ravi.

He was saving ₹5,000 a month in a savings account. He had no clear financial goal beyond “maybe buy a bike someday.” He believed investing was for people who “understood the market,” and he wasn’t one of them.

Then he asked himself a question Schwartz poses early in the book:

“What would I do if I knew I could not fail?”

Arjun’s answer: I’d build a ₹1 crore corpus, buy a flat, and retire early.

The next question: What’s stopping me?

His answer: Nothing except my own thinking.

So he changed how he thought.

Instead of “I can’t afford ₹10,000/month SIPs,” he asked, “How can I afford ₹10,000/month SIPs?”

Instead of “Investing is risky,” he asked, “What’s the risk of NOT investing?”

Instead of “₹1 crore is impossible,” he asked, “What would it take to make ₹1 crore possible?”

And once he started asking better questions, the answers appeared.

He cut unnecessary expenses. He upskilled and switched jobs for a 30% raise. He started a SIP with ₹8,000, then stepped it up every year. He surrounded himself with people who invested, not people who complained about money.

Five years later, Arjun’s portfolio is worth ₹9.8 lakhs and growing. He’s on track to hit ₹1 crore in another 10 years—maybe sooner if he keeps stepping up his SIPs.

Ravi? Still saving in his account. Still hoping “someday” he’ll have enough.

—

What This Series Will Cover

Over the next 12 articles, we’re going to break down the core principles of The Magic of Thinking Big and apply them directly to your financial life.

You’ll learn: – How to eliminate the excuses that keep you from investing (Article 3) – How to build confidence by taking small, consistent actions (Article 4) – How to set ambitious financial goals without feeling overwhelmed (Article 5) – How to think creatively about earning and saving more (Article 6) – How to shift your money identity from spender to wealth-builder (Article 7) – How to manage your environmentto surround yourself with the right influences (Article 8) – How to turn market crashes into opportunitiesinstead of disasters (Article 9) – How to leverage relationships for career and income growth (Article 10) – How to develop the action habit that turns plans into reality (Article 11) – How to turn financial setbacks into stepping stones (Article 12)

Each article will feature real stories, practical steps, and Indian financial context—SIPs, mutual funds, term insurance, emergency funds, the works.

By the end of this series, you won’t just understand The Magic of Thinking Big. You’ll have applied it to your money and seen the results.

—

The Magic Isn’t in the Book. It’s in You.

Here’s the secret David Schwartz doesn’t spell out directly, but it’s woven into every page:

You already have everything you need to build wealth. You have access to mutual funds, SIPs, compounding, and time. The tools are there. The opportunity is there.

What’s missing isn’t knowledge. It’s permission.

Permission to think bigger than ₹10,000 in savings. Permission to set a goal like ₹1 crore and actually believe it’s possible. Permission to start small, make mistakes, and keep going anyway.

This series gives you that permission.

Arjun didn’t become a crorepati overnight. He became someone who thinks like a crorepati. And that shift—from small thinking to big thinking—is what changed everything.

Your financial future doesn’t start with a salary hike or a windfall. It starts in your mind.

So here’s the question:

How big are you willing to think?

—

Next in the series: “I’ll Never Be Rich”: How One Belief Keeps You Poor (And How to Change It)

—

Disclaimer: This article is for educational purposes only. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. The author is a SEBI-registered Mutual Fund Distributor (ARN 351164). Past performance is not indicative of future returns.