Chapters 9, 10 · How to Use the Will · Further Use of the Will

This is Article 4 of the “Science of Getting Rich × Mutual Funds” series on rahulmoney.com

Here is a question worth sitting with: How many people do you know who fully understand that they should be investing in mutual funds — and still aren’t?

Probably several. Maybe you were one of them until recently. Maybe you still are, in some areas.

This is the central problem Wallace Wattles tackles in Chapters 9 and 10. He calls it the proper use of the will. His argument: the will is not primarily a tool for resisting temptation or forcing yourself to do hard things through sheer grit. The will is best used to direct your attention and action toward what matters — and to keep it there, steadily, without being derailed by fear, distraction, or social noise.

Why intelligent people don’t invest

It is rarely a knowledge problem. Most salaried professionals who are not investing already know they should be. The gap is not information. It is activation.

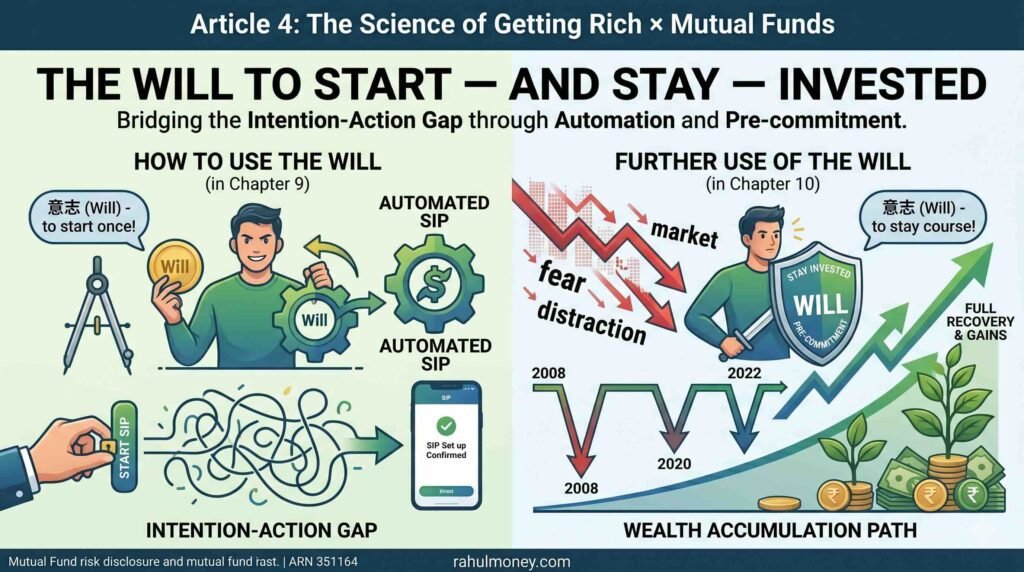

Behavioural economists call this the intention-action gap. You intend to start a SIP. You tell yourself you will do it after the next appraisal, or once you clear the credit card balance, or when you understand it better. Months become years. The compounding clock ticks quietly without you.

The will, used correctly, closes this gap. Not by forcing yourself into something uncomfortable — but by making the action automatic, so willpower is no longer required.

Automation is the highest use of financial will

The most powerful financial decision most salaried professionals can make is not which fund to pick. It is to automate their SIP so that investing happens without any decision being required each month.

When your SIP is automated: you never have to feel ready. You never have to check if the market is at a good level. You never have to remember to invest. The money moves before you can spend it. This is willpower deployed once to eliminate the need for willpower every month.

The automation principle: Set it up once. Let it run. Your future self will thank your present self for removing every opportunity to make the wrong decision.

Staying invested when everything says to stop

Chapter 10 addresses the further use of the will — specifically, maintaining your direction when external pressure pushes against it. In investing, that pressure arrives as market crashes.

The Nifty 50 fell approximately 52% in the 2008 financial crisis. It fell 38% in March 2020 during the COVID pandemic. It fell meaningfully in 2022 during global rate hike fears. Each time, the news cycle was full of experts warning of deeper falls, prolonged pain, and permanent loss.

Investors who stayed invested — who used their will to maintain direction rather than react to the noise — experienced full recovery and significant gains on every single occasion. The 2020 recovery was so swift that investors who stopped their SIPs in March missed one of the fastest bull runs in Indian market history.

Staying invested is not passive. It is an active choice, made again and again in the face of fear. That is exactly what Wattles means by the further use of the will.

Your two decisions this week

- If you do not have an automated SIP: set one up today. Choose a fund, set the date, link your bank account. Do it before you finish reading this article.

- If you already have a SIP: commit, in writing, to what it would take for you to stop it. Make the conditions specific and high — not “if the market falls 20%” but “if my goal fundamentally changes.” This pre-commitment protects you from emotional decisions.

Mutual Fund investments are subject to market risks. Please read all scheme related documents carefully before investing. ARN: 351164 | rahulmoney.com