Chapter 13 · Getting Into the Right Business

This is Article 6 of the “Science of Getting Rich × Mutual Funds” series on rahulmoney.com

There is a wealth gap that most salaried professionals never talk about. Not the gap between the rich and the poor. The gap between what your income could build — and what it actually builds.

Consider a software professional earning Rs. 15 lakh per annum at age 28. Over the next decade, with normal career progression, they might see their CTC grow to Rs. 35-40 lakh. That is a significant income. Potentially a life-changing income. But if lifestyle inflation keeps pace with every salary hike — a bigger flat, a better car, more subscriptions, more dining out — the wealth gap stays exactly where it started. More income, same savings rate. Higher salary, same financial position.

What Wattles knew: your income source matters

Chapter 13 of The Science of Getting Rich is about getting into the right business — aligning your work with your potential so that your income can grow with your contribution. For most salaried professionals, this translates to career growth: developing skills that command higher pay, taking on more responsibility, building expertise that is genuinely valuable.

But Wattles was also pointing at something subtler. Your career is your primary wealth-generation engine. The fuel it produces — your monthly salary — is only valuable if some of it is converted into assets before it disappears into expenses.

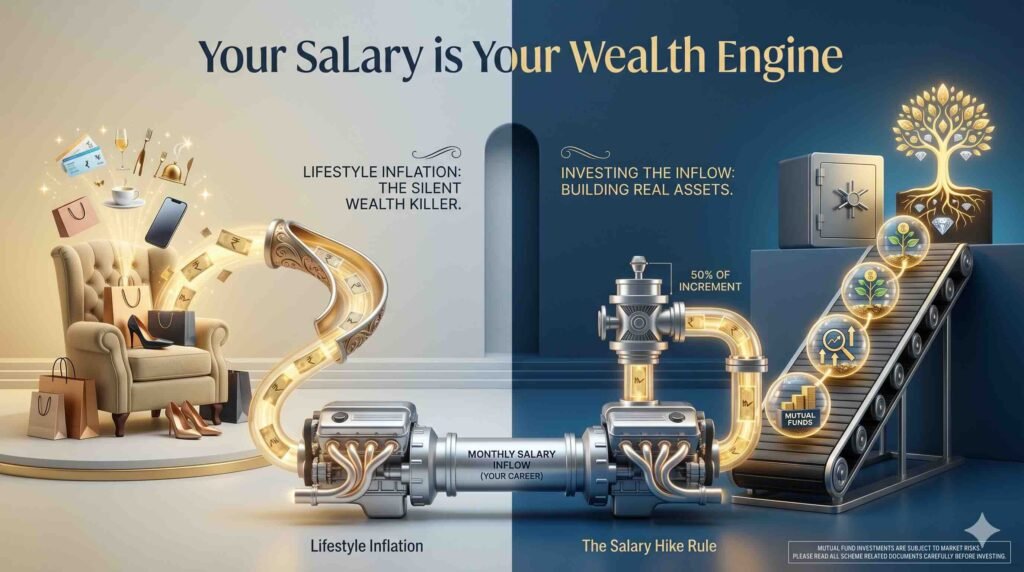

The formula is simple: Income – Investments = Lifestyle Budget. Not the other way around.

The salary hike rule: Every time your salary increases, increase your SIP by at least 50% of the increment. If your take-home rises by Rs. 10,000, move Rs. 5,000 into a new or existing SIP before your lifestyle adapts to the higher income. Your lifestyle will adjust. Your future corpus will thank you.

Lifestyle inflation: the silent wealth killer

Lifestyle inflation is not a character flaw. It is a natural human tendency. When you earn more, you want to live better. There is nothing wrong with that. The problem is when the entire increment goes toward consumption and nothing goes toward investment.

The salaried professional who earns Rs. 10 lakh and invests Rs. 1 lakh per year is building wealth. The one who earns Rs. 30 lakh and invests nothing is not — regardless of how impressive their salary sounds at a dinner party.

Income events to always invest from

- Annual salary increment: increase SIP by at least 50% of the monthly take-home increase.

- Performance bonus: put at least 30-50% into a lump sum top-up in your existing fund.

- Promotion: open a new SIP goal or increase the target for an existing one.

- Tax refund: invest it. You did not budget for it; do not spend it.

- Any windfall: Diwali bonus, incentive payout, freelance income — at least half goes to investments.

Your career is your most powerful financial asset in your 20s and 30s. Make sure its output goes into building real assets, not just a more expensive lifestyle.

Mutual Fund investments are subject to market risks. Please read all scheme related documents carefully before investing. ARN: 351164 | rahulmoney.com